Author:

The purpose of this article is to build a predictive model for Mergers and Acquisitions (M&A) target identification and discover if that will produce an abnormal return for investors by utilizing Refinitiv Data APIs. Extensive literature review is conducted to identify main Machine Learning models as well as variables used in empirical studies which can be provided by individual request. The rest of the article is structured in the following way. Section 1 briefly provides theoretical background to M&A, discusses the main motivations and drivers, and suggests main stakeholders who can benefit from target predictive modeling. Section 2 and Section 3 present the methodology of predictive modeling and describe the data respectively. Section 4 discusses the empirical results from logistic regression models and identifies significant variables. We test out-of sample predictive power of the models in Section 5. Section 6 provides portfolio return estimations based on the prediction outputs.

Content

- Theoretical Background

1.1 Definitions to M&A

1.2 Background to M&A

- Methodology

2.1 Methodology of the predictive model

2.2 Methodology for portfolio abnormal returns estimation

- Data description

3.1 Dataset for Target companies

3.2 Dataset for non-Target companies

- Empirical results

4.1 Variables selection

4.2 Results from Logistic regression models

4.2.1 Model on the entire dataset

4.2.2 Model on the clustered dataset

4.2.3 Comparison of unclustered and clustered results: The effect of clustering

- Out of sample predictive power of the model

5.1 Identification of optimal cut-off probability

5.2 Classification results on the holdout sample

5.2.1 Results from the model on the entire dataset

5.2.2 Results from the models on seperate clusters

- Portfolio returns

6.1 Announcement returns

6.2 Portfolio returns

6.2.1 Portfolio abnormal returns

6.2.2 Portfolio investment returns

- Conclusion

Below are three code cells containing packages required in this report. If these packages are not already installed on your computer, please run these cells.

!pip install eikon

!pip install sklearn

!pip install seaborn

!pip install plotnine

!pip install openpyxl

import numpy as np

import pandas as pd

import os

import seaborn as sns

import plotnine as pn

import datetime

from sklearn.linear_model import LogisticRegression

from sklearn.linear_model import LinearRegression

from sklearn import metrics

from sklearn import preprocessing

from sklearn.metrics import accuracy_score, f1_score, precision_score, recall_score

from sklearn.cluster import KMeans

from sklearn.datasets import make_classification

from sklearn.metrics import roc_curve

from sklearn.metrics import roc_auc_score

from numpy import mean

from numpy import std

from sklearn.model_selection import KFold

from sklearn.model_selection import StratifiedKFold

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import RepeatedKFold

import statsmodels.api as sm

from statsmodels.stats.outliers_influence import variance_inflation_factor

from scipy.stats import ttest_ind

from plotnine import *

# import eikon package and read app key from a text file

import eikon as ek

app_key = open("app_key.txt","r")

ek.set_app_key(app_key.read())

app_key.close()

Section 1: Theoretical Background

1.1 Definitions to M&A

M&A are corporate actions involving restructuring and change of control within companies, which play an essential role in external corporate growth. The literature uses the terms of mergers, acquisitions, and takeovers synonymously; however, there are subtle differences in their economic implications. Piesse, Lee, Lin, and Kuo (2013) interpret acquisitions and takeovers as activities when the acquirer gets control over 50% equity of the target company and mergers when two firms join to form a new entity.

Overall, according to Piesse et al. (2013), the negotiating process is often friendly in M&A, assuming synergies for both firms and hostile in case of takeovers. In this sense, terms “merger” and “acquisition” are used synonymously to refer to friendly corporate actions and “takeovers” to hostile corporate actions. The current article concentrates on friendly M&A only, which assumes a substantial premium for the target’s stock price.

1.2 Background to M&A

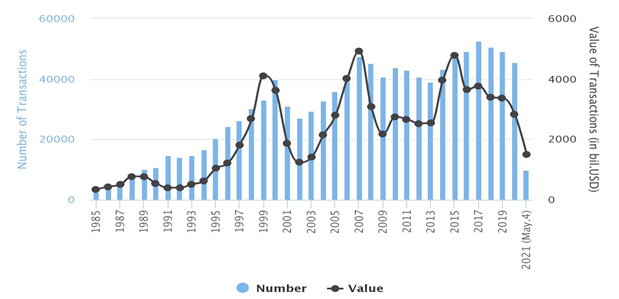

M&A activity has increased throughout recent years both in terms of the number and value of the deals. The number of M&A deals reached its peak in 2017 when 50,600 M&A deals were announced, totaling USD 3.5 trillion. The activity was more than twenty times higher than the number of deals in 1985 and around ten times higher than the deal value for the same year. M&A activity for 1985-2021 is summarized in Figure below (Source):

M&A activity is evolving in cycles that coincide with the economic rise and major shocks, such as the IT bubble in the 2000s, the financial crisis in 2007-2009, and recent economic movements caused by COVID-19. These tendencies are well researched in academic literature and are referred to as merger waves (Martynova & Renneboog, 2006). Mitchell and Mulherin (1996) claim that M&A activity is driven by industry and macroeconomic shocks, which trigger the start or end of M&A activity waves triggered by regulatory, economic, or technological shocks and innovations.

1.3 Main stakeholders of M&A prediction modeling

Tunyi (2021) suggests three stakeholders interested in predicting M&A targets:

Investors - Corporate events, such as M&A or bankruptcy announcements, result in substantial stock price changes, thus allowing investors to receive abnormal returns. Previous research reports significant abnormal returns for target companies. For example, Jensen and Ruback (1983) claim 29.1% weighted average abnormal return for target companies in the US in the two months around the M&A announcement.

Company managers - Prior academic literature considers management inefficiency one of the main factors of a company’s acquisition. Thus, knowledge of anticipated takeover allows taking the necessary actions to safeguard shareholder interests by setting up takeover defense strategies (Tunyi, 2021). Those strategies may make the takeover deal unattractive or allow the managers and target company shareholders to generate excess returns (Schwert, 2000). Additionally, information on the probability of the company’s partners’ and competitors’ engagement in M&A could be helpful in the company’s strategy development (Tunyi, 2021).

Regulators An essential role of securities market regulators is to identify and exclude insider trading. Keown and Pinkerton (1981) mention that many individuals and groups, such as bankers, advisers who are engaged in M&A, hold non-public price-sensitive information, which is poorly kept secret. Several researchers (Schwert, 1996; Goergen & Renneboog, 2004) identify stock price run-ups from two to four months before announcing the M&A. While Jensen and Ruback (1983) explain that by market anticipation, Keown and Pinkerton (1981), Schwert (1996) attribute it to insider trading. A practical tool allowing regulators to investigate the extent of market anticipation of takeover based on public information could help them make informed decisions on market abuse

Researchers used various empirical techniques for target identification, including parametric, linear discriminant analysis, conditional and logistical regression, and non-parametric techniques, such as SVM, Neural Networks, and Utilities Additive Discriminants. Despite the wide range of methodologies, logistic regression was proven to be the most prevailing due to higher classification accuracy and the explainability of the outputs. We have also tested different methodologies, including SVM, Decision tree, Random forest algorithms and identify that logistic regression generalizes better and provides higher accuracy and explainability.

Thus, in line with most previous empirical studies, the current article uses logistic regression to classify target and non-target companies.Intermediate clustering of sample data is employed to test whether prediction accuracy and abnormal returns will increase.

Logistic Regression: The study uses binary logistic regression and is conducted in Python using the sklearn package with a liblinear solver and penalty of l2 (ridge regression). The model equation is given as follows:

$$ \begin{array}{ll} {P}_{i} = \frac{1}{1 + e^{-z_i}} \end{array}$$

${P}_{i}$ is the probability of company ${i}$ being a target, and ${Z}_{i}$ is the vector of the company ${i}$ characteristics given as the following:

$$ \begin{array}{ll} {Z}_{i} = {β_0} + {β_1}{X_1} + {β_2}{X_2} + {β_3}{X_3} + {β_n}{X_n} + {ε_i} \end{array}$$

where ${β_0}$ is the intercept and ${β_j}$(${j}$ = 1,…,${k}$) is the coefficient of respective independent variable ${X_j}$ (j = 1,…,k) for each company. The dependent dummy variable equals to 1 if the company is a target and 0 otherwise. It is worth highlighting that all the variables are sourced as of 1 month before the announcement, both for target and non-target groups. Non-targets are matched with targets as of the announcement date of the corresponding target acquisition.

To identify the optimal variables to include in the logistic regression model and avoid multicollinearity, correlation analysis, t-test for the mean difference, and Variance Inflation Factor (VIF) test are used. First, correlation analysis was done to identify the interdependence of the variables and potential multicollinearity. One of the correlated variables was eliminated based on its significance in the t-test and VIF score.

Clustering: Further, we propose a clustering technique to test if that increases the accuracy of logistic regression outputs and portfolio returns. We compared prediction outputs and portfolio returns between logistic regression models estimated on the entire and clustered datasets to test this. We started by estimating logistic regression on the entire dataset. Then, we clustered the entire dataset into two groups and evaluated logistic regression models on each cluster separately. Finally, we compared results from models based on the entire dataset and each cluster dataset. Additionally, combined clustered outputs were compared with the results from the entire dataset.

The clustering is done based on liquidity and leverage variables of target and non-target companies, which are the same as in logistic regression. The study uses the Kmeans clustering technique conducted in a Python environment using the sklearn package.

The algorithm is an iterative process aimed to partition data into prespecified groups to minimize the sum of the squared distance (Euclidean distance in our case) between the data points and the cluster centroid (Hastie, Tibshirani, & Friedman,2009).The algorithm aims to minimize the following equation:

$$ \begin{array}{ll} {J} = \sum \limits_{j=1} ^ {k} \sum \limits_{i=1} ^ {n}{||{x_i}^{(j)}- {c_j}||^{2}} \end{array}$$

where ${j}$ is the number of clusters, which is 2 in our case, ${i}$ is the number of sample companies ${x_i}^{(j)}$ is the company ${i}$ for cluster ${j}$ and ${c_j}$ is the centroid for cluster ${j}$.

Portfolio construction Strategies

To estimate the practical usefulness of the target prediction model an optimal cut-off based on the maximization of the difference between True Positive Rate (TPR) and False Positive Rate (FPR) is used to classify target and non-target companies.

Then, portfolio abnormal returns for an observation period of 60 days before and 3 days after the announcement for all predicted target companies are calculated. Additionally, an investment strategy of buying all predicted targets during the beginning of the year and selling right after the announcement (false predicted targets are kept in the portfolio until the end of the observation period) is employed. The portfolio investment return is compared with Standard & Poor’s (S&P) 500 return for the same period to identify whether the portfolio constructed from all predicted targets can generate market excess return.

Calculation of abnormal returns

Abnormal returns are calculated by using event study methodology (MacKinlay,1997) using the following equation.

$$ \begin{array}{ll} {AR}_{i,t} = {r_{i,t}} - {(α_i + β_i R_{m,t})} \end{array}$$

where ${r_{i,t}}$ is the return on security ${i}$ in period ${t}$, ${R_{m,t}}$ is the market return in period ${t}$. ${α}$ and ${β}$ are model parameters. ${α}$ is a constant that assumed zero; ${β}$ is calculated by regressing stock returns against the market returns and shows stock returns volatility versus the market returns.

The methodology assumes an estimation period when model parameters, such as ${β}$ is estimated and an observation period for which the actual returns are calculated. ${β}$ is calculated for the estimation period by regressing daily stock returns against the S&P 500 index as a market return proxy. Further, to calculate Cumulative Abnormal Return (CAR), abnormal returns of each stock are summed for the whole observation period:

$$ \begin{array}{ll} {CAR}_{(t_1,t_2)} = \sum \limits_{t=t_1} ^ {t_2} {AR_{it}} \end{array}$$

where, ${t_1}$,${t_2}$ denote the start and the end of the observation period.

The following function calculates abnormal return of a given security during an observation period based on Event study Methodology(MacKinlay,1997).

def ab_return(RIC, sdate, edate, announce_date, period):

'''

Calculate abnormal return of a given security during an observation period based on Event study Methodology(MacKinlay,1997)

Dependencies

------------

Python library 'eikon' version 1.1.12

Python library 'numpy' version 1.20.1

Python library 'pandas' version 1.2.4

Python library 'Sklearn' version 0.24.1

Parameters

-----------

Input:

RIC (str): Refinitiv Identification Number (RIC) of a stock

sdate (str): Starting date of the estimation period - in yyyy-mm-dd

edate (str): End date of the estimation period, which is also starting date of the observation period - in yyyy-mm-dd

announce_date (str): End date of the observation period which is assumed to be the M&A announcment date or any other specified date

period (int): Number of trading days in during the observation period. For each date in this period abnormal return is calculated

Output:

CAR (int): Cumulative Abnormal Return (CAR) for a given stock

abnormal_returns (DataFrame): Dataframe containing abnormal returns during the observation period

'''

#create an empty dataframe to store abnormal returns

abnormal_returns = pd.DataFrame({'#': np.arange(start = 1, stop = period)})

## estimate linear regression model parameters based on estimation period

# get timeseries for the specified RIC and market proxy (S&P 500 in our case) for the both estimation and observation period

df_all_per = ek.get_timeseries([RIC, '.SPX'],

start_date = sdate,

end_date = announce_date,

interval='daily',

fields = 'CLOSE')

# slice the estimation period

df_all_per.reset_index(inplace = True)

df_est_per = df_all_per.loc[(df_all_per['Date'] <= edate)]

# calculate means of percentage change of returns for the stock and market proxy

df_est_per.insert(loc = len(df_est_per.columns), column = "Return_stock", value = df_est_per[RIC].pct_change()*100)

df_est_per.insert(loc = len(df_est_per.columns), column = "Return_market", value = df_est_per[".SPX"].pct_change()*100)

mean_stock = df_est_per["Return_stock"].mean()

mean_index = df_est_per["Return_market"].mean()

df_est_per.dropna(inplace = True)

# reshape the dataframe and estimate parameters of linear regression

y = df_est_per["Return_stock"].to_numpy().reshape(-1,1)

X = df_est_per["Return_market"].to_numpy().reshape(-1,1)

model = LinearRegression().fit(X,y)

Beta = model.coef_[0][0]

intercept = model.intercept_[0]

# slice the estimation period

df_obs_per = df_all_per.loc[(df_all_per['Date'] >= edate)]

# calculate percentage change of returns for the stock and market proxy

df_obs_per.insert(loc = len(df_obs_per.columns), column = "Return_stock", value = df_obs_per[RIC].pct_change()*100)

df_obs_per.insert(loc = len(df_obs_per.columns), column = "Return_market", value = df_obs_per[".SPX"].pct_change()*100)

df_obs_per.dropna(inplace=True)

df_obs_per.reset_index(inplace=True)

# calculate and return cumulative abnormal return (CAR) for the observation period

abnormal_returns.insert(loc = len(abnormal_returns.columns), column = str(RIC)+'_Date', value = df_obs_per["Date"])

abnormal_returns.dropna(inplace=True)

abnormal_returns.insert(loc = len(abnormal_returns.columns), column = str(RIC)+'_return', value = df_obs_per["Return_stock"] - (intercept + Beta * df_obs_per["Return_market"]))

CAR = abnormal_returns.iloc[:,2].sum()

return CAR, abnormal_returns

The following gives an example of calculaing abnormal return for Slack Technologies (WORK.N^G21) during the observation period which includes the aquisition announcement date by Salesforce.

CAR, abnormal_returns = ab_return("WORK.N^G21", '2020-03-26', "2020-10-02", "2020-12-01", 60)

CAR

50.620286227582014

The function mentioned above has been used to calculate abnormal returns for 3 different cases:

1. Calculate Run-up return vriable for target and non-target companies - This variable is based on the findings in the previous literature (Keown & Pinkerton, 1981, Barnes, 1998), suggesting that target companies generate significant run-up returns during one to two months before the announcement of the deal. We calculate this return for both target and non-target companies.The period 250 to 60 days before the deal announcement was used as an estimation window. The observation period was two months before the announcement.

2. Calculate post announcement abnormal returns - In order to support the assumption that shareholders of target companies receive abnormal returns after company acquisition post-announcement abnormal returns for target companies are calculated.

3. Calculate portfolio abnormal returns - abnormal returns for the portfolios, constructed based on the models outputs are calculated to test whether a target prediction model can capture some of the examined announcement abnormal returns.

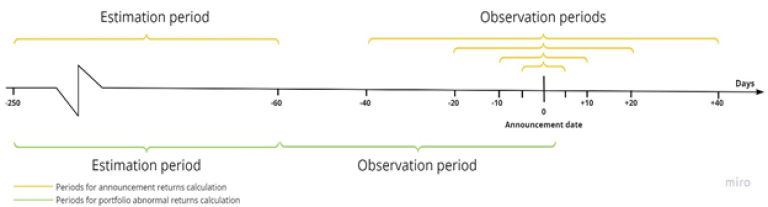

The estimation window for both the announcement and portfolio returns is 250 to 60 days before the deal announcement. The observation period for portfolio abnormal return calculation is 60 days before and 3 days after the announcement. As for the announcement returns, multiple observation periods, such as [-40, +40], [-20, +20], [-10, +10], [-5, +5], are considered to observe both run-up (two months preceding the announcement) and mark-up returns (two months following the deal announcement). The Figure below illustrates observation and estimation periods of both announcement and portfolio abnormal returns.

To build a logistic regression model for target prediction a dataset of target and non-target companies is required. Two separate datasets for each group of companies is retrieved from Refinitiv and then merged into single one with appropriate labels to estimate a Logistic regression model.

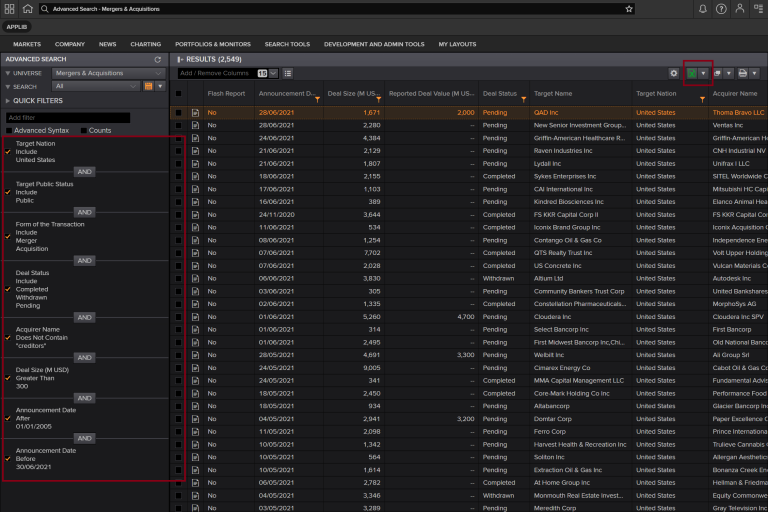

The target sample is constructed based on M&A Advanced Search section of Refinitiv Workspace to include relevant deals for target companies in the US. The screen shot below shows the filters used to get the relevant data for the article.

The retrieved data consisted of 2549 target companies from the US. Further screening for data availability of selected variables (1547 observations eliminated), peers (254 observations eliminated), and removal of outliers (92 observations eliminated) resulted in a final dataset of 656 target companies for announcement date from April 2010 – June 2021. The final dataset for target companies is included in the github folder of the current article. As the data were retrieved in excel from the Advanced Search directly we retrieve variable values directly in excel using Refinitiv Add-in formulas.

The following code reads the target dataset into a dataframe.

#read target group dataset from excel file: update URL based on your file location

target_group = pd.read_excel (r'Target_Sample.xlsx')

#select only the columns needed for the subsequect sections

target_group = target_group.iloc[:,3:31]

target_group.head()

| AD-30 | Announcement Date | Company RIC | Market Cap | Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| 0 | 29/05/2021 | 28/06/2021 | QADA.O | 1.28E+09 | -9.77544 | 10.77455 | 4.201914 | 59.18308 | 0.077847 | 4.544522 | ... | 4.807378 | 4.129297 | 11.42875 | 0.097879 | 0.996802 | 1.002554 | -6.27018 | -0.9134 | 1 | 1 |

| 1 | 22/05/2021 | 21/06/2021 | RAVN.O | 1.16E+09 | -7.70184 | 7.449319 | 6.531071 | 33.81626 | 0.0565 | 7.288653 | ... | 4.424246 | 4.337533 | 4.644855 | 0.008242 | 0.180739 | 0.098591 | -0.84217 | -0.09042 | 1 | 1 |

| 2 | 22/05/2021 | 21/06/2021 | LDL | 5.33E+08 | -11.8431 | -4.71313 | -1.55563 | 18.96168 | -0.1396 | 2.823379 | ... | 0.813417 | 1.031316 | 2.430913 | 1.049446 | 32.00883 | 0.193466 | 9.432784 | 0.3186 | 1 | 1 |

| 3 | 19/05/2021 | 18/06/2021 | SYKE.OQ^H21 | 1.49E+09 | -11.1465 | 7.669254 | 3.841362 | 32.09241 | 0.058989 | 7.49143 | ... | 0.931876 | 0.895016 | 1.780169 | 0.070497 | 3.052414 | 0.107747 | -1.44018 | -0.05943 | 0 | 1 |

| 4 | 09/05/2021 | 08/06/2021 | MCF | 3.98E+08 | -9.64752 | -251.266 | -146.448 | 8.89214 | -5.3374 | -20.0788 | ... | 7.253047 | 7.377276 | 45.87027 | 0.989979 | 1.849967 | 0.044645 | 0.080742 | 0.45284 | 0 | 1 |

target_group.describe()

| Market Cap | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | ROC | EV/EBIDTA | Sales growth, 3y | Free cash Flow/Sales | ... | Working Capital to Total Assests | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | |

| count | 6.56E+02 | 656 | 656 | 656 | 655 | 656 | 656 | 656 | 656 | 656 | ... | 655 | 6.56E+02 | 656 | 656 | 656 | 656 | 655 | 656 | 656 | 656 |

| mean | 4.05E+09 | 1.227193 | 0.004292 | 42.592205 | 0.011263 | 8.386456 | 7.23945 | 10.709083 | 16.277893 | -0.005295 | ... | 0.192846 | 2.57E+00 | 3.179511 | 4.055075 | 1.278185 | 26.890114 | 0.1747 | 9.272178 | 0.160276 | 0.317073 |

| std | 8.61E+09 | 51.640629 | 33.771662 | 21.314522 | 0.264163 | 20.842951 | 13.043522 | 59.78252 | 55.207696 | 0.453567 | ... | 0.210179 | 2.74E+00 | 3.113478 | 6.783922 | 3.441966 | 22.710054 | 0.223336 | 15.630188 | 0.47266 | 0.465691 |

| min | 1.14E+07 | -764.000937 | -256.188448 | 0.56503 | -5.337401 | -245.91966 | -72.692063 | -864.301773 | -25.870643 | -6.586436 | ... | -0.67105 | 8.00E-09 | 0.095067 | -1.557987 | -35.141609 | 0 | 0.000072 | -23.83771 | -2.62278 | 0 |

| 25% | 5.95E+08 | -1.868845 | -1.386343 | 26.123918 | -0.008542 | 2.897525 | 3.257199 | 7.013958 | 0.924596 | -0.010343 | ... | 0.02784 | 8.14E-01 | 1.163568 | 1.604212 | 0.154095 | 6.051583 | 0.029994 | -0.964812 | -0.122802 | 0 |

| 50% | 1.42E+09 | 6.999636 | 3.864721 | 41.146985 | 0.039185 | 8.911569 | 7.353025 | 10.612786 | 7.095638 | 0.051043 | ... | 0.15772 | 1.74E+00 | 2.235609 | 2.447625 | 0.738462 | 24.968875 | 0.099197 | 5.778312 | 0.29549 | 0 |

| 75% | 3.94E+09 | 14.453616 | 9.865902 | 57.78912 | 0.088947 | 17.107852 | 12.727209 | 16.922002 | 17.110155 | 0.115698 | ... | 0.30882 | 3.33E+00 | 3.874402 | 4.047843 | 1.325697 | 42.010874 | 0.232926 | 15.229821 | 0.51408 | 1 |

| max | 1.05E+11 | 246.345515 | 205.474778 | 99.23579 | 0.536342 | 59.360426 | 59.537746 | 440.269908 | 976.508129 | 0.661562 | ... | 0.86214 | 2.70E+01 | 19.02814 | 103.5282 | 41.333135 | 131.325927 | 2.622785 | 166.992527 | 1.17803 | 1 |

The non-target sample was constructed from companies similar to target companies first, in terms of business activity, and second, size as measured by market capitalization at the time of the bid. To identify the non-target control group, Refinitiv peers SCREEN is used. The Peer group for each company and the variables to be used in the prediction model are retrieved using the function in the cell below.

def peers(RIC, date):

'''

Get peer group for an individual RIC along with required variables for the models

Dependencies

------------

Python library 'eikon' version 1.1.12

Python library 'pandas' version 1.2.4

Parameters

-----------

Input:

RIC (str): Refinitiv Identification Number (RIC) of a stock

date (str): Date as of which peer group and variables are requested - in yyyy-mm-dd

Output:

peer_group (DataFrame): Dataframe of 50 peer companies along with requested variables

'''

# specify variables for the request

fields=["TR.TRBCIndustry", "TR.TRBCBusinessSector", "TR.TRBCActivity", "TR.F.MktCap", "TR.F.ReturnAvgTotEqPctTTM",

"TR.F.IncAftTaxMargPctTTM","TR.F.GrossProfMarg","TR.F.NetIncAfterMinIntr","TR.F.TotCap","TR.F.OpMargPctTTM",

"TR.F.ReturnCapEmployedPctTTM","TR.F.NetCashFlowOp", "TR.F.LeveredFOCF", "TR.F.TotRevenue", "TR.F.RevGoodsSrvc3YrCAGR",

"TR.F.NetPPEPctofTotAssets", "TR.F.TotAssets","TR.F.SGA","TR.F.CurrRatio","TR.F.WkgCaptoTotAssets",

"TR.PriceToBVPerShare","TR.PriceToSalesPerShare","TR.EVToEBITDA","TR.EVToSales","TR.F.TotShHoldEq","TR.F.TotDebtPctofTotAssets",

"TR.F.DebtTot","TR.F.NetDebtPctofNetBookValue","TR.F.NetDebttoTotCap","TR.TotalDebtToEV","TR.F.NetDebtPerShr","TR.TotalDebtToEBITDA"]

#search for peers

instruments = 'SCREEN(U(IN(Peers("{}"))))'.format(RIC)

#request variable data for each peer

peer_group, error = ek.get_data(instruments = instruments, fields = fields, parameters = {'SDate': date})

# df.to_excel(str(RIC[i]) + '.xlsx') - can be enabled if required to store peer data in excel

return peer_group

The following gives an example of retrieving peers and specified variables for Slack Technologies. The next cell provides the list of target company RICs along with the date for peer identification and variable retrieval.

#request peer data for Slack and show first 5 peers

peers('WORK.N^G21', '2020-11-01').head()

| Instrument | TRBC Industry Name | TRBC Business Sector Name | TRBC Activity Name | Market Capitalization | Return on Average Total Equity - %, TTM | Income after Tax Margin - %, TTM | Gross Profit Margin - % | Net Income after Minority Interest | Total Capital | ... | Enterprise Value To EBITDA (Daily Time Series Ratio) | Enterprise Value To Sales (Daily Time Series Ratio) | Total Shareholders' Equity incl Minority Intr & Hybrid Debt | Total Debt Percentage of Total Assets | Debt - Total | Net Debt Percentage of Net Book Value | Net Debt to Total Capital | Total Debt To Enterprise Value (Daily Time Series Ratio) | Net Debt per Share | Total Debt To EBITDA (Daily Time Series Ratio) | |

| 0 | CRM.N | IT Services & Consulting | Software & IT Services | Cloud Computing Services | 1.61709E+11 | 8.53505 | 12.244582 | 75.23102 | 126000000 | 36947000000 | ... | 75.667295 | 10.56531 | 33885000000 | 5.55455 | 3062000000 | -16.84483 | -0.13222 | 1.305458 | -5.470325 | 0.987805 |

| 1 | TEAM.OQ | Software | Software & IT Services | Software (NEC) | 44700285864 | -63.864982 | -25.815988 | 83.34708 | -350654000 | 1729057000 | ... | 348.861618 | 27.320632 | 575306000 | 29.62839 | 1153751000 | <NA> | -0.57558 | 2.479368 | -4.021923 | 8.649564 |

| 2 | SPLK.OQ | Software | Software & IT Services | Software (NEC) | 24215811839 | -41.714537 | -27.622625 | 81.78035 | -336668000 | 3714059000 | ... | <NA> | 13.637515 | 1999429000 | 31.522 | 1714630000 | -2.06907 | -0.01091 | 7.035879 | -0.256871 | <NA> |

| 3 | NOW.N | Software | Software & IT Services | Enterprise Software | 53245552000 | 34.148025 | 16.597748 | 76.97849 | 626698000 | 2822922000 | ... | 179.616716 | 22.703498 | 2127941000 | 11.53988 | 694981000 | -88.00939 | -0.35287 | 1.779752 | -5.25762 | 3.196732 |

| 4 | MSFT.OQ | Software | Software & IT Services | Software (NEC) | 1.54331E+12 | 41.399328 | 32.285167 | 67.781 | 44281000000 | 1.91127E+11 | ... | 21.371859 | 9.968566 | 1.18304E+11 | 24.16872 | 72823000000 | -116.67399 | -0.33331 | 5.026813 | -8.414212 | 1.074323 |

# retrieve RICs and dates for target group companies

RICs = target_group['Company RIC'].to_list()

date = target_group['AD-30'].dt.strftime('%Y-%m-%d').to_list()

Running "peer" function over all RICs and dates above will create dataframes (or excel files) for each target company, which will include all peers along with specified variables. After screening the peer data based on their similarity to the target group and data availability, each target was matched by year with the closest non-target company.The final dataset for non-target companies is included in the github folder of the current article.

non_target_group = pd.read_excel (r'Non-target_sample.xlsx')

non_target_group = non_target_group.iloc[:,4:31]

non_target_group.head()

| Announcement Date | Company RIC | Market Cap | Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | Return on Capital | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| 0 | 28/06/2021 | OPRA.OQ | 1.04E+09 | -2.831319 | 6.083762 | 65.461049 | 83.82711 | 0.169373 | 15.307199 | 1.39486 | ... | 7.262251 | 6.548395 | 1.296834 | 0.008555 | 0.735752 | 0.126564 | -1.101874 | -0.11889 | 0 | 0 |

| 1 | 21/06/2021 | BDGI.TO | 1.33E+09 | -7.522057 | 1.43515 | 0.894579 | 15.33098 | 0.052053 | 1.9545 | 1.837 | ... | 2.575443 | 2.793027 | 4.468704 | 0.447268 | 8.701365 | 0.036376 | 3.719562 | 0.27267 | 0 | 0 |

| 2 | 21/06/2021 | LXFR.N | 4.54E+08 | -4.183324 | 12.733008 | 6.93408 | 24.90764 | 0.090703 | 11.847015 | 12.007564 | ... | 1.998172 | 2.126281 | 3.635942 | 0.319569 | 10.675449 | 0.006803 | 1.789655 | 0.23537 | 1 | 0 |

| 3 | 18/06/2021 | CSGS.OQ | 1.48E+09 | -1.351786 | 13.953294 | 5.693989 | 43.61389 | 0.075892 | 10.941099 | 13.94227 | ... | 1.472389 | 1.61714 | 3.443384 | 0.831489 | 21.661849 | 0.243919 | 3.390701 | 0.14338 | 1 | 0 |

| 4 | 08/06/2021 | NOG.A | 4.02E+08 | 22.048509 | -329.504482 | -388.580768 | 4.88476 | -1.255706 | 15.533732 | 4.011939 | ... | 1.826714 | 3.535152 | -3.433331 | -4.231196 | 48.400209 | 0.001979 | 20.549773 | 1.3075 | 0 | 0 |

non_target_group.describe()

| Market Cap | Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | Return on Capital | EV to EBIDTA | Sales growth, 3y | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| count | 6.56E+02 | 656 | 656 | 656 | 656 | 656 | 656 | 656 | 656 | 656 | ... | 6.56E+02 | 656 | 656 | 656 | 656 | 656 | 656 | 656 | 656 | 656 |

| mean | 4.33E+09 | -0.03835 | 5.461099 | 3.032561 | 42.11838 | 0.045924 | 9.690908 | 9.461485 | 13.03909 | 18.25903 | ... | 3.06E+00 | 3.688036 | 3.90387 | 1.040082 | 23.00153 | 0.168167 | 9.464655 | 0.11195 | 0.335366 | 0 |

| std | 9.40E+09 | 17.67915 | 37.75587 | 29.40039 | 22.05762 | 0.161203 | 22.55952 | 14.18395 | 71.4611 | 54.84517 | ... | 3.98E+00 | 4.877811 | 9.202817 | 2.782451 | 21.69162 | 0.19202 | 32.38858 | 0.43166 | 0.472478 | 0 |

| min | 9.15E+06 | -126.719 | -456.588 | -388.581 | -13.2379 | -1.25571 | -263.836 | -71.0716 | -801.847 | -27.3662 | ... | 6.40E-08 | 0.097714 | -57.4275 | -4.2312 | 0 | 0 | -155.537 | -1.58058 | 0 | 0 |

| 25% | 6.39E+08 | -8.06732 | 1.434235 | 1.063125 | 24.7642 | 0.007688 | 4.223528 | 4.037114 | 7.515283 | 1.190327 | ... | 7.73E-01 | 1.062764 | 1.450024 | 0.108651 | 4.598596 | 0.031875 | -1.47364 | -0.18771 | 0 | 0 |

| 50% | 1.59E+09 | 0.176899 | 8.971992 | 5.342759 | 40.22623 | 0.053812 | 9.181608 | 8.680717 | 11.16064 | 7.887975 | ... | 1.66E+00 | 2.087322 | 2.408813 | 0.538702 | 18.37021 | 0.10329 | 2.629143 | 0.188925 | 0 | 0 |

| 75% | 4.09E+09 | 8.888801 | 16.61211 | 10.67219 | 57.44022 | 0.101982 | 17.32304 | 15.17464 | 18.00727 | 18.29859 | ... | 3.79E+00 | 4.29108 | 4.139631 | 1.054455 | 35.62091 | 0.241191 | 12.27956 | 0.438397 | 1 | 0 |

| max | 9.36E+10 | 135.3732 | 157.6795 | 100.8545 | 100 | 0.969145 | 85.14702 | 115.929 | 689.3331 | 879.8665 | ... | 4.18E+01 | 65.16187 | 183.2269 | 47.82671 | 127.4428 | 1.601634 | 435.7095 | 1.3075 | 1 | 0 |

Hereof, data from 2010-2019 are used as a training sample for the prediction model, and data from 2020-2021 as a hold-out testing sample to measure the prediction outputs. Finally, other non-target companies from peer data (all peers were included based on data availability) were added in the hold-out sample to have a similar to natural world distribution of target and non-target companies. The all target sample consisting of 1705 observations is stored in github folder of this article.

non_target_all = pd.read_excel (r'non-target_all.xlsx')

non_target_all = non_target_all.iloc[:,4:31]

non_target_all.head()

| Announcement Date | Company RIC | Market Cap | Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | Return on Capital | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| 0 | 28/06/2021 | ORCL.N | 1.70E+11 | -2.326304 | 104.657802 | 32.324708 | 77.64155 | 0.122175 | 39.064271 | 17.34117 | ... | 5.720429 | 6.58138 | 25.612618 | 5.628686 | 26.528822 | 0.441759 | 9.299967 | 0.33836 | 0 | 0 |

| 1 | 28/06/2021 | APPF.OQ | 6.18E+09 | 5.841547 | 76.413277 | 49.575963 | 52.97011 | 0.554012 | 0.40571 | 0.434931 | ... | 14.705474 | 14.237565 | 16.26181 | 0 | 0 | 0.490567 | -4.900518 | -0.58939 | 0 | 0 |

| 2 | 28/06/2021 | APPS.O | 3.76E+08 | -3.597121 | 45.866903 | 15.068955 | 38.693 | 0.141264 | 17.909776 | 47.794993 | ... | 22.945682 | 22.850398 | 52.729386 | 0.270393 | 0.322305 | 0.218848 | -0.006771 | -0.00601 | 0 | 0 |

| 3 | 28/06/2021 | SPSC.OQ | 3.83E+09 | 1.688433 | 11.630102 | 14.084168 | 66.29434 | 0.108352 | 15.610047 | 12.147986 | ... | 10.245945 | 9.611462 | 7.640845 | 0 | 0 | 0.355799 | -5.282973 | -0.44561 | 1 | 0 |

| 4 | 28/06/2021 | OPRA.OQ | 1.04E+09 | -1.893117 | 6.083762 | 65.461049 | 83.82711 | 0.169373 | 15.307199 | 1.39486 | ... | 7.262251 | 6.548395 | 1.296834 | 0.008555 | 0.735752 | 0.126564 | -1.101874 | -0.11889 | 0 | 0 |

Training dataset

Final training dataset consisting of target and non-target companies is created by merging target and non target group dataset and selecting only the observations before 2020-01-01. This is used to train the logistic regression model for target identification.

data = pd.concat([target_group, non_target_group], ignore_index=True)

#select only observations earlier than January 1, 2020 for the trainig dataset

data = data.loc[data["Announcement Date"] < "2020-01-01"]

data.head()

| AD-30 | Announcement Date | Company RIC | Market Cap | Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| 75 | 19/10/2019 | 18/11/2019 | SDI^G20 | 2.59E+08 | 18.90802 | 13.07202 | 3.033754 | 47.29568 | 0.007028 | 17.38898 | ... | 0.524636 | 1.178682 | 3.958383 | 2.576265 | 48.9193 | 0.062581 | 11.274 | 0.5609 | 1 | 1 |

| 85 | 24/11/2019 | 24/12/2019 | AXE^F20 | 1.80E+09 | 10.58003 | 12.19726 | 2.32083 | 19.29359 | 0.055382 | 4.238786 | ... | 0.335002 | 0.448346 | 1.684529 | 0.797122 | 27.73048 | 0.028701 | 34.57491 | 0.41485 | 1 | 1 |

| 86 | 23/11/2019 | 23/12/2019 | WAAS.K^C20 | 5.05E+08 | 4.173605 | -5.32525 | -10.2765 | 53.22647 | -0.03158 | 3.50351 | ... | 3.49148 | 4.571051 | 1.66549 | 0.949824 | 36.04978 | 0.086268 | 9.82416 | 0.40087 | 0 | 1 |

| 87 | 20/11/2019 | 20/12/2019 | CRCM.K^B20 | 6.25E+08 | 22.87365 | -12.0777 | -9.43021 | 76.91928 | 0.245749 | -3.10547 | ... | 1.940667 | 1.582142 | 2.401903 | 0 | 0 | 0.429477 | -3.97826 | -0.59256 | 1 | 1 |

| 88 | 19/11/2019 | 19/12/2019 | TIVO.O^F20 | 1.17E+09 | 2.869971 | -30.7963 | -71.75 | 48.63371 | -0.14058 | 3.716264 | ... | 1.376742 | 2.33317 | 0.704931 | 0.664552 | 58.92102 | 0.065171 | 5.414204 | 0.2701 | 0 | 1 |

Testing dataset

Predictive power of the model is estimated on the hold-out sample consisting of target group observations after 2020-01-01 and all non-target peer companies.

#create holdout testing sample by joining target group observations dating after January 1, 2020 and all non-target observationa

data_hold = pd.concat([target_group.loc[target_group["Announcement Date"] > "2020-01-01"], non_target_all], ignore_index=True)

data_hold.head()

| AD-30 | Announcement Date | Company RIC | Market Cap | Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| 0 | 29/05/2021 | 28/06/2021 | QADA.O | 1.28E+09 | -9.775437 | 10.77455 | 4.201914 | 59.18308 | 0.077847 | 4.544522 | ... | 4.807378 | 4.129297 | 11.428748 | 0.097879 | 0.996802 | 1.002554 | -6.270184 | -0.9134 | 1 | 1 |

| 1 | 22/05/2021 | 21/06/2021 | RAVN.O | 1.16E+09 | -7.701835 | 7.449319 | 6.531071 | 33.81626 | 0.0565 | 7.288653 | ... | 4.424246 | 4.337533 | 4.644855 | 0.008242 | 0.180739 | 0.098591 | -0.842171 | -0.09042 | 1 | 1 |

| 2 | 22/05/2021 | 21/06/2021 | LDL | 5.33E+08 | -11.843083 | -4.71313 | -1.555628 | 18.96168 | -0.139595 | 2.823379 | ... | 0.813417 | 1.031316 | 2.430913 | 1.049446 | 32.008828 | 0.193466 | 9.432784 | 0.3186 | 1 | 1 |

| 3 | 19/05/2021 | 18/06/2021 | SYKE.OQ^H21 | 1.49E+09 | -11.146474 | 7.669254 | 3.841362 | 32.09241 | 0.058989 | 7.49143 | ... | 0.931876 | 0.895016 | 1.780169 | 0.070497 | 3.052414 | 0.107747 | -1.440183 | -0.05943 | 0 | 1 |

| 4 | 09/05/2021 | 08/06/2021 | MCF | 3.98E+08 | -9.647523 | -251.26627 | -146.447928 | 8.89214 | -5.337401 | -20.078817 | ... | 7.253047 | 7.377276 | 45.870267 | 0.989979 | 1.849967 | 0.044645 | 0.080742 | 0.45284 | 0 | 1 |

# report number of observations and structure of the datasets

print(f"Number of target companies in training dataset is: {data.loc[data['Label']==1].shape[0]}")

print(f"Number of non-target companies in training dataset is: {data.loc[data['Label']==0].shape[0]}")

print(f"\nNumber of target companies in hold-out testing dataset is: {data_hold.loc[data_hold['Label']==1].shape[0]}")

print(f"Number of non-target companies in hold-out testing dataset is: {data_hold.loc[data_hold['Label']==0].shape[0]}")

Number of target companies in training dataset is: 572

Number of non-target companies in training dataset is: 572

Number of target companies in hold-out testing dataset is: 84

Number of non-target companies in hold-out testing dataset is: 1704

This section discusses the variable selection process and presents empirical results from the logistic regression models.

#select numeric fields only

data = data.iloc[:,4:29]

# run t-test

t_test = ttest_ind(data.loc[data['Label']==1], data.loc[data['Label']==0])

#store results in a dataframe

ttest_data = pd.DataFrame()

ttest_data["feature"] = data.columns

ttest_data["t_test"] = t_test[0]

ttest_data["p-value"] = t_test[1]

ttest_data = ttest_data.T

ttest_data.rename(columns = ttest_data.iloc[0], inplace = True)

ttest_data = ttest_data.iloc[1:]

ttest_data

| Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | Return on Capital | EV to EBIDTA | Sales growth, 3y | Free cash Flow/Sales | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| t_test | 3.527428 | -1.475911 | -1.889791 | 0.444909 | -2.945529 | -0.931712 | -2.840692 | -1.111184 | -0.657753 | 0.860847 | ... | -1.973785 | -1.756332 | -0.395142 | 1.511998 | 3.23238 | 0.074497 | -0.596586 | 1.742697 | -0.941765 | inf |

| p-value | 0.000436 | 0.140243 | 0.059039 | 0.656469 | 0.003289 | 0.351683 | 0.004582 | 0.266723 | 0.51083 | 0.389503 | ... | 0.048647 | 0.0793 | 0.692812 | 0.130811 | 0.001263 | 0.940628 | 0.550902 | 0.081656 | 0.346512 | 0 |

# create dataframe to store VIF scores

vif_data = pd.DataFrame()

vif_data["feature"] = data.columns

vif_data

# calculate VIF for each feature

vif_data["VIF"] = [variance_inflation_factor(data.values, i)

for i in range(len(data.columns))]

vif_data = vif_data.T

vif_data.rename(columns = vif_data.iloc[0], inplace = True)

vif_data = vif_data.iloc[1:]

vif_data

| Abnormal return 60 day | ROE | Profit Margin | Gross Profit Margin | Profit to Capital | Return on Sales | Return on Capital | EV to EBIDTA | Sales growth, 3y | Free cash Flow/Sales | ... | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| VIF | 1.054777 | 1.881072 | 2.665773 | 6.042009 | 3.554314 | 5.010072 | 5.76416 | 1.157921 | 1.311202 | 2.419423 | ... | 20.179892 | 23.487542 | 2.079249 | 2.184374 | 6.102144 | 4.116519 | 1.609153 | 5.965589 | 1.933686 | 2.065807 |

#provide correlation matrix of variables

data.corr(method ='pearson')

| Profit to Capital | Return on Sales | Return on Capital | EV to EBIDTA | Sales growth, 3y | Free cash Flow/Sales | Operating cash flow to Total Assets | Asset Turnover | Current Ratio | Working Capital to Total Assests | Price to Sales | EV to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Net debt to Total Capital | Growth-Resource Mismatch | Label | |

| Profit to Capital | 1 | 0.469819 | 0.770463 | 0.057058 | -0.099643 | 0.159629 | 0.571263 | 0.133556 | -0.026975 | -0.023155 | -0.092609 | -0.095129 | 0.000116 | -0.061493 | -0.194562 | -0.062241 | -0.058041 | -0.01065 | 0.093123 | -0.086833 |

| Return on Sales | 0.469819 | 1 | 0.571258 | 0.072925 | -0.125538 | 0.304241 | 0.475287 | -0.160287 | -0.208076 | -0.256022 | -0.025165 | 0.084847 | -0.02229 | 0.02147 | 0.063414 | -0.236161 | 0.113287 | 0.220759 | -0.040704 | -0.02756 |

| Return on Capital | 0.770463 | 0.571258 | 1 | 0.072687 | -0.103096 | 0.184553 | 0.640436 | 0.250245 | -0.108058 | -0.080304 | -0.165991 | -0.146214 | 0.02568 | 0.001541 | -0.121035 | -0.126193 | -0.00914 | 0.103537 | 0.069217 | -0.083765 |

| EV to EBIDTA | 0.057058 | 0.072925 | 0.072687 | 1 | -0.031775 | -0.216339 | 0.050431 | -0.019283 | -0.020741 | -0.055012 | 0.142681 | 0.187297 | 0.021269 | 0.003807 | 0.003469 | -0.075433 | 0.01399 | 0.082962 | -0.001593 | -0.032864 |

| Sales growth, 3y | -0.099643 | -0.125538 | -0.103096 | -0.031775 | 1 | -0.230891 | -0.080419 | -0.08697 | 0.135151 | 0.095959 | 0.198016 | 0.196634 | 0.04208 | -0.035913 | -0.04864 | 0.082146 | -0.011732 | -0.111481 | -0.091704 | -0.01946 |

| Free cash Flow/Sales | 0.159629 | 0.304241 | 0.184553 | -0.216339 | -0.230891 | 1 | 0.287205 | 0.130224 | 0.024008 | 0.08932 | -0.393878 | -0.542854 | 0.023437 | -0.027909 | -0.123641 | 0.084361 | -0.068922 | -0.105306 | 0.056599 | 0.025465 |

| Operating cash flow to Total Assets | 0.571263 | 0.475287 | 0.640436 | 0.050431 | -0.080419 | 0.287205 | 1 | 0.237074 | -0.072218 | -0.030645 | -0.129507 | -0.1691 | 0.050883 | -0.046929 | -0.275411 | 0.047895 | -0.111884 | -0.121877 | 0.064638 | -0.023641 |

| Asset Turnover | 0.133556 | -0.160287 | 0.250245 | -0.019283 | -0.08697 | 0.130224 | 0.237074 | 1 | -0.021046 | 0.198435 | -0.367556 | -0.443685 | 0.016387 | -0.049528 | -0.194819 | 0.084507 | -0.158973 | -0.118254 | 0.141162 | -0.00063 |

| Current Ratio | -0.026975 | -0.208076 | -0.108058 | -0.020741 | 0.135151 | 0.024008 | -0.072218 | -0.021046 | 1 | 0.805576 | 0.180575 | -0.001214 | 0.003018 | -0.139586 | -0.333796 | 0.331163 | -0.257875 | -0.475517 | 0.320242 | 0.012113 |

| Working Capital to Total Assests | -0.023155 | -0.256022 | -0.080304 | -0.055012 | 0.095959 | 0.08932 | -0.030645 | 0.198435 | 0.805576 | 1 | 0.09664 | -0.122366 | 0.040904 | -0.170173 | -0.460793 | 0.515196 | -0.329673 | -0.661775 | 0.413097 | 0.011728 |

| Price to Sales | -0.092609 | -0.025165 | -0.165991 | 0.142681 | 0.198016 | -0.393878 | -0.129507 | -0.367556 | 0.180575 | 0.09664 | 1 | 0.905159 | 0.21278 | -0.088396 | -0.262439 | 0.190755 | -0.080365 | -0.226254 | -0.096225 | -0.058308 |

| EV to Sales | -0.095129 | 0.084847 | -0.146214 | 0.187297 | 0.196634 | -0.542854 | -0.1691 | -0.443685 | -0.001214 | -0.122366 | 0.905159 | 1 | 0.149185 | -0.016209 | -0.031145 | -0.007317 | 0.072198 | 0.020936 | -0.147149 | -0.051902 |

| Market to Book | 0.000116 | -0.02229 | 0.02568 | 0.021269 | 0.04208 | 0.023437 | 0.050883 | 0.016387 | 0.003018 | 0.040904 | 0.21278 | 0.149185 | 1 | 0.48869 | -0.077159 | 0.139582 | -0.079884 | -0.014592 | -0.027932 | -0.011692 |

| Total debt to Equity | -0.061493 | 0.02147 | 0.001541 | 0.003807 | -0.035913 | -0.027909 | -0.046929 | -0.049528 | -0.139586 | -0.170173 | -0.088396 | -0.016209 | 0.48869 | 1 | 0.394115 | -0.12604 | 0.251266 | 0.381659 | -0.10333 | 0.044698 |

| Debt to EV | -0.194562 | 0.063414 | -0.121035 | 0.003469 | -0.04864 | -0.123641 | -0.275411 | -0.194819 | -0.333796 | -0.460793 | -0.262439 | -0.031145 | -0.077159 | 0.394115 | 1 | -0.409302 | 0.469554 | 0.725694 | -0.238567 | 0.095216 |

| Cash to Capital | -0.062241 | -0.236161 | -0.126193 | -0.075433 | 0.082146 | 0.084361 | 0.047895 | 0.084507 | 0.331163 | 0.515196 | 0.190755 | -0.007317 | 0.139582 | -0.12604 | -0.409302 | 1 | -0.309905 | -0.719857 | 0.167972 | 0.002204 |

| Net debt per share | -0.058041 | 0.113287 | -0.00914 | 0.01399 | -0.011732 | -0.068922 | -0.111884 | -0.158973 | -0.257875 | -0.329673 | -0.080365 | 0.072198 | -0.079884 | 0.251266 | 0.469554 | -0.309905 | 1 | 0.4629 | -0.094465 | -0.017651 |

| Net debt to Total Capital | -0.01065 | 0.220759 | 0.103537 | 0.082962 | -0.111481 | -0.105306 | -0.121877 | -0.118254 | -0.475517 | -0.661775 | -0.226254 | 0.020936 | -0.014592 | 0.381659 | 0.725694 | -0.719857 | 0.4629 | 1 | -0.264913 | 0.051501 |

| Growth-Resource Mismatch | 0.093123 | -0.040704 | 0.069217 | -0.001593 | -0.091704 | 0.056599 | 0.064638 | 0.141162 | 0.320242 | 0.413097 | -0.096225 | -0.147149 | -0.027932 | -0.10333 | -0.238567 | 0.167972 | -0.094465 | -0.264913 | 1 | -0.027857 |

| Label | -0.086833 | -0.02756 | -0.083765 | -0.032864 | -0.01946 | 0.025465 | -0.023641 | -0.00063 | 0.012113 | 0.011728 | -0.058308 | -0.051902 | -0.011692 | 0.044698 | 0.095216 | 0.002204 | -0.017651 | 0.051501 | -0.027857 | 1 |

Variables for the logistic regression model are selected through triangulation of results from correlation matrix, t-test analysis, and VIF estimates. Variables are presented into 6 groups which describe different aspect of a company:

Inefficient Management: (ROE, ROC, Return on Sales, Profit Margin, Gross Profit Margin, Profit to Capital, Sales Growts(3y))

We identify that Gross Profit Margin and Sales growth are not correlated with any of the variables, thus included in the final model. The most correlated variables are Profit to Capital, ROC, and ROE, which is logical considering the components of the ratios. Considering comparably higher t-test and lower VIF scores, Profit to Capital is selected for the final model. As another highly correlated variable with the Profit to Capital ratio, Profit Margin was also eliminated from the list. Return on Sales, along with Profit to Capital, Gross Profit Margin, and Sales Growth, was the fourth variable considered for the model as a proxy for inefficient management.

Company undervaluation: (P/E, EV to Sales, EV to EBITDA, Market to Book)

Moving to variables describing company undervaluation, EV to EBITDA, and M/B ratios are not correlated with the rest of the variables and are included in the model. In contrast, EV to Sales and Price to Sales is highly correlated with each other. Considering the greater difference in t-test and lower VIF score of Price to Sales ratio, EV to Sales was eliminated from the list of final variables.

Growth-resource Imbalance: (Growth-Resource Mismatch, Free Cash Flow to Sales, Operating Cash Flow to Total Assets)

Free cash flow to Sales and Operating cash flow to Total Assets are other correlated variables. Both describe Growth-resource Imbalance, and based on the above-described considerations, only Free cash flow to sales was included in the model. Dummy of imbalance was included as a proxy for Growth-resource Mismatch.

Leverage: (Total Debt to Equity, Debt to EV, Net Debt per Share, Net Debt to Total Capital)

Debt to EV, Net Debt to Total Capital variables are highly correlated. Only Debt to EV was included in the final model considering its higher significant mean difference. More variables proxying Leverage are Net Debt-based ratios. Only Net debt per share was selected because of the high correlation between Net Debt to Total Capital and other variables (including Debt to EV, Cash to Capital) considered for the model.

Liquidity: (Current Ratio, Cash to Capital, Working Capital to Total Assets)

As for the variables describing liquidity, both the Current and Cash to Capital ratios were included in the model. Working Capital to Total Assets is eliminated because of its high correlation with the current ratio and higher VIF score.

Run-up returns: (Abnormal Return previous 60 days)

Lastly, the t-test of Abnormal return is significant at the 1% level. The mean difference is in line with our hypothesis, suggesting that target companies have higher run-up returns. The abnormal return is not correlated with any observed variables, thus included in the final model.

# remove specified variables and prepare final dataset for the logistic regression model

drop = ['Return on Capital',"EV to Sales","Working Capital to Total Assests",

'Operating cash flow to Total Assets','Asset Turnover',

'Net debt to Total Capital','Profit Margin', 'ROE']

data.drop(columns=drop, inplace=True)

data.head()

| Abnormal return 60 day | Gross Profit Margin | Profit to Capital | Return on Sales | EV to EBIDTA | Sales growth, 3y | Free cash Flow/Sales | Current Ratio | Price to Sales | Market to Book | Total debt to Equity | Debt to EV | Cash to Capital | Net debt per share | Growth-Resource Mismatch | Label | |

| 75 | 18.908016 | 47.29568 | 0.007028 | 17.388983 | 6.624964 | 23.607172 | -0.006725 | 1.54999 | 0.524636 | 3.958383 | 2.576265 | 48.919298 | 0.062581 | 11.274002 | 1 | 1 |

| 85 | 10.580031 | 19.29359 | 0.055382 | 4.238786 | 9.964724 | 11.032365 | 0.011345 | 1.93994 | 0.335002 | 1.684529 | 0.797122 | 27.730476 | 0.028701 | 34.574912 | 1 | 1 |

| 86 | 4.173605 | 53.22647 | -0.031583 | 3.50351 | 31.02985 | 13.336855 | 0.049832 | 2.47767 | 3.49148 | 1.66549 | 0.949824 | 36.049779 | 0.086268 | 9.82416 | 0 | 1 |

| 87 | 22.873645 | 76.91928 | 0.245749 | -3.105473 | 30.648062 | 11.566996 | 0.16575 | 3.1974 | 1.940667 | 2.401903 | 0 | 0 | 0.429477 | -3.978257 | 1 | 1 |

| 88 | 2.869971 | 48.63371 | -0.140578 | 3.716264 | 9.784327 | 11.620528 | 0.1911 | 0.97639 | 1.376742 | 0.704931 | 0.664552 | 58.921021 | 0.065171 | 5.414204 | 0 | 1 |

Three different logistic regression models are estimated. First logistic regression is estimated on the entire dataset (Model 1). Then the entire dataset is divided into two clusters based on liquidity and leverage ratios of target and non-target companies, and logistic regression is run on each cluster separately (Model 2 and 3). Model outputs are discussed thereof.

First, we create separate dataframes for independent and dependent variables

X = data.drop(['Label','Total debt to Equity'],axis =1)

y = data['Label']

# fit logistic regression model on the unclustered dataset

lr = LogisticRegression(solver = 'liblinear',penalty = 'l2', random_state=0)

lr.fit(X, y)

# fit logistic regression model by different package to show the summary output

log_reg = sm.Logit(y, X).fit()

print(log_reg.summary())

| Optimization | terminated | successfully. | ||||||

| Current | function | value: | 0.676776 | |||||

| Iterations | 5 | |||||||

| Logit | Regression | Results | ||||||

| Dep. Variable: | Label | No. Observations: | 1144 | |||||

| Model: | Logit | Df Residuals: | 1130 | |||||

| Method: | MLE | Df Model: | 13 | |||||

| Date: | Tue, 14 Sep 2021 | Pseudo R-squ.: | 0.02362 | |||||

| Time: | 22:01:50 | Log-Likelihood: | -774.23 | |||||

| converged: | TRUE | LL-Null: | -792.96 | |||||

| Covariance Type: | nonrobust | LLR p-value: | 0.0003512 | |||||

| coef | std err | z | P>|z| | [0.025 | 0.975] | |||

| Abnormal | return | 60 day | 0.0118 | 0.004 | 3.012 | 0.003 | 0.004 | 0.019 |

| Gross | Profit | Margin | 0.0031 | 0.003 | 1.03 | 0.303 | -0.003 | 0.009 |

| Profit | to | Capital | -1.2249 | 0.526 | -2.329 | 0.02 | -2.256 | -0.194 |

| Return | on | Sales | -0.0007 | 0.004 | -0.164 | 0.87 | -0.009 | 0.008 |

| EV | to | EBIDTA | -0.0009 | 0.001 | -0.801 | 0.423 | -0.003 | 0.001 |

| Sales | growth, | 3y | -0.0012 | 0.002 | -0.724 | 0.469 | -0.005 | 0.002 |

| Free | cash | Flow/Sales | 0.0524 | 0.189 | 0.278 | 0.781 | -0.317 | 0.422 |

| Current | Ratio | 0.0186 | 0.038 | 0.49 | 0.624 | -0.056 | 0.093 | |

| Price | to | Sales | -0.0512 | 0.028 | -1.848 | 0.065 | -0.106 | 0.003 |

| Market | to | Book | -0.0003 | 0.008 | -0.04 | 0.968 | -0.017 | 0.016 |

| Debt | to | EV | 0.007 | 0.003 | 2.402 | 0.016 | 0.001 | 0.013 |

| Cash | to | Capital | -0.0586 | 0.375 | -0.156 | 0.876 | -0.794 | 0.677 |

| Net | debt | per share | -0.0053 | 0.003 | -1.707 | 0.088 | -0.011 | 0.001 |

| Growth-Resource | Mismatch | -0.1516 | 0.139 | -1.094 | 0.274 | -0.423 | 0.12 |

The results suggest statistically significant output for Abnormal returns in 1%, Profit to capital, Debt to EV ratios in 5%, and Price to Sales, Net debt per share variables in 10% significance level. Moreover, the coefficient of Profit to Capital is negative, confirming the hypothesis of inefficient management, suggesting that underperforming firms are more likely to be acquired. The firm undervaluation hypothesis is confirmed and aligns with previous studies as companies with low Price to Sales ratios are significantly associated with target companies. The results could not claim the hypothesis of Growth-Resource imbalance and Liquidity for none of the variables in observed significance levels. In contrast, the hypothesis on Leverage is confirmed for both observed variables, in 5% and 10% significance levels, respectively.

Moreover, the coefficient of Debt to EV is positive, suggesting that target firms have higher leverage, in line with the previous studies. On the contrary, Net debt per share coefficient is negative, which contradicts the hypothesis and previous studies. A possible explanation is that the ratio excludes cash and cash equivalents from the debt, which may suggest that the observed target companies have higher liquidity in terms of cash. Finally, Abnormal return over the previous 60 days is highly significant with a positive coefficient allowing to claim the hypothesis that target companies generate positive abnormal run-up returns.

Next we hypothesize that Clustering companies before classification improves prediction accuracy. This hypothesis is based on our intuition and is motivated by the findings in the literature that companies in financial distress (lower-liquid or high-levered) have a higher probability of being acquired. Acquisitions of financially distressed companies are mainly related to disciplinary takeovers where a target is acquired because of poor performance. The acquirer is usually a financial buyer seeking mainly financial returns by improving the company’s financial health. However, there is also synergetic acquisition where the acquirer looks for synergies with the target company to improve its business operations. In this case, the target companies are not necessarily financially distressed; moreover, they usually have high growth opportunities. Thus, the characteristics of target companies in disciplinary and synergetic acquisitions are different; therefore, different variables may explain their acquisition likelihood. To test this hypothesis, we employed a clustering algorithm based on sample companies’ liquidity and leverage ratios and run separate logistic regression models on each of the two clusters.

# keep only leverage and liquidity ratios

cl_drop = ['Label','Free cash Flow/Sales','Growth-Resource Mismatch','EV to EBIDTA','Abnormal return 60 day', 'Return on Sales',

'Gross Profit Margin','Price to Sales','Market to Book','Total debt to Equity','Sales growth, 3y','Profit to Capital']

dat_cl = data.drop(cl_drop, axis = 1)

# run kmeans algorithm and partition data into two clusters

km = KMeans(n_clusters = 2).fit(dat_cl)

# store cluster values in a dataframe

cluster_map = pd.DataFrame()

cluster_map['data_index'] = dat_cl.index.values

cluster_map['cluster'] = km.labels_

# create list of indexes for each cluster

cl_0_idx = []

cl_1_idx = []

for i in range(len(dat_cl)):

if cluster_map.iloc[i,1] == 0:

cl_0_idx.append(i)

if cluster_map.iloc[i,1] == 1:

cl_1_idx.append(i)

print("Number of elements in Cluster 0 is" , len(cl_0_idx))

print("Number of elements in Cluster 1 is" , len(cl_1_idx))

Number of elements in Cluster 0 is 702

Number of elements in Cluster 1 is 442

# plot distribution of target and non-target companies in each cluster

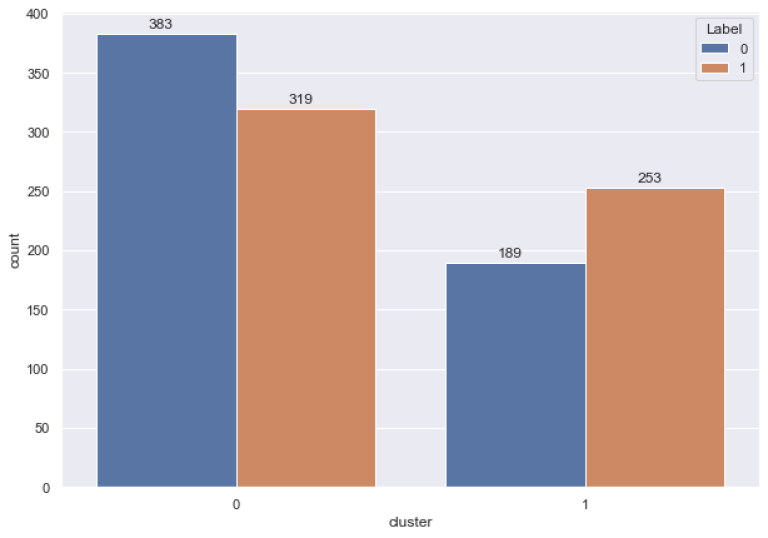

cluster_map["Label"] = y.values

sns.set(rc = {'figure.figsize':(10,7)})

ax = sns.countplot(x = "cluster", hue = "Label", data = cluster_map)

# add numeric values on the bars

for p in ax.patches:

ax.annotate('{:.0f}'.format(p.get_height()), (p.get_x() + 0.15, p.get_height() + 5))

The table below summarizes cluster centroids for each cluster per variable. It is evident from the results that companies in Cluster 0 have higher liquidity and lower leverage. On the contrary, Cluster 1 companies are in a worse financial condition in terms of long-term leverage and short-term financial power.

# get cluster centroids

cl_centroid = km.cluster_centers_

# store variable centroids in a dataframe

centroids = pd.DataFrame()

centroids["Variable"] = dat_cl.columns

centroids["Mean_cluster 0"] = cl_centroid[0]

centroids["Mean_cluster 1"] = cl_centroid[1]

centroids

| Variable | Mean_cluster 0 | Mean_cluster 1 | |

| 0 | Current Ratio | 2.805736 | 1.554494 |

| 1 | Debt to EV | 10.621829 | 47.207315 |

| 2 | Cash to Capital | 0.23208 | 0.065443 |

| 3 | Net debt per share | 0.236114 | 24.964022 |

Further we run logistic regression models on each cluster datapoints and discuss the results

lr_0 = LogisticRegression(solver = 'liblinear',random_state=0, penalty = 'l2')

lr_0.fit(X.iloc[cl_0_idx], y.iloc[cl_0_idx])

log_reg = sm.Logit(y.iloc[cl_0_idx], X.iloc[cl_0_idx]).fit()

print(log_reg.summary())

| Optimization | terminated | successfully. | ||||||

| Current | function | value: | 0.670424 | |||||

| Iterations | 6 | |||||||

| Logit | Regression | Results | ||||||

| Dep. | Variable: | Label No. Observations: | 702 | |||||

| Model: | Logit | Df Residuals: | 688 | |||||

| Method: | MLE | Df Model: | 13 | |||||

| Date: | Tue, 14 Sep 2021 | Pseudo R-squ.: | 0.02694 | |||||

| Time: | 22:02:05 | Log-Likelihood: | -470.64 | |||||

| converged: | TRUE | LL-Null: | -483.67 | |||||

| Covariance Type: | nonrobust | LLR p-value: | 0.01668 | |||||

| coef | std err | z | P>|z| | [0.025 | 0.975] | |||

| Abnormal | return | 60 day | 0.014 | 0.005 | 2.648 | 0.008 | 0.004 | 0.024 |

| Gross | Profit | Margin | 0.0036 | 0.004 | 0.941 | 0.347 | -0.004 | 0.011 |

| Profit | to | Capital | -1.4259 | 0.663 | -2.152 | 0.031 | -2.725 | -0.127 |

| Return | on | Sales | 0.0059 | 0.007 | 0.862 | 0.388 | -0.008 | 0.019 |

| EV | to | EBIDTA | -0.0012 | 0.001 | -0.975 | 0.33 | -0.003 | 0.001 |

| Sales | growth, | 3y | -0.0051 | 0.003 | -1.68 | 0.093 | -0.011 | 0.001 |

| Free | cash | Flow/Sales | -0.0313 | 0.375 | -0.083 | 0.934 | -0.766 | 0.703 |

| Current | Ratio | 0.0321 | 0.046 | 0.692 | 0.489 | -0.059 | 0.123 | |

| Price | to | Sales | -0.0672 | 0.038 | -1.779 | 0.075 | -0.141 | 0.007 |

| Market | to | Book | -0.0026 | 0.023 | -0.112 | 0.911 | -0.049 | 0.043 |

| Debt | to | EV | -0.0177 | 0.008 | -2.144 | 0.032 | -0.034 | -0.002 |

| Cash | to | Capital | 0.6774 | 0.457 | 1.482 | 0.138 | -0.218 | 1.573 |

| Net | debt | per share | 0.0324 | 0.017 | 1.949 | 0.051 | 0 | 0.065 |

| Growth-Resource | Mismatch | -0.1303 | 0.175 | -0.744 | 0.457 | -0.473 | 0.213 |

Logistic regression outputs from Cluster 0, which includes companies in better financial health, find similar results to Model based on the entire dataset. Particularly, Abnormal returns are significant in 1%, Profit to capital, Debt to EV ratios in 5%, and Price to Sales at a 10% significance level. In addition, Net debt per share is also significant at a 5% level. The directions of the impact of significant variables are mainly similar to the first model; however, the coefficient values are higher for the Cluster 1 model for all variables. The exception is leverage ratios, where the direction of coefficients is the opposite, suggesting that companies with lower Debt to EV and higher Net debt per share contribute to the acquisition.

lr_1 = LogisticRegression(solver = 'liblinear',random_state=0, penalty = 'l2')

lr_1.fit(X.iloc[cl_1_idx], y.iloc[cl_1_idx])

log_reg = sm.Logit(y.iloc[cl_1_idx], X.iloc[cl_1_idx]).fit()

print(log_reg.summary())

| Optimization |

terminated | successfully. | |||||||

| Current | function | value: | 0.648109 | ||||||

| Iterations | 6 | ||||||||

| Logit | Regression | Results | |||||||

| Dep. Variable: | Label | No. Observations: | 442 | ||||||

| Model: | Logit | Df Residuals: | 428 | ||||||

| Method: | MLE | Df Model: | 13 | ||||||

| Date: | Tue, 14 Sep 2021 | Pseudo R-squ.: | 0.05057 | ||||||

| Time: | 22:02:10 | Log-Likelihood: | -286.46 | ||||||

| converged: | TRUE | LL-Null: | -301.72 | ||||||

| Covariance Type: | nonrobust | LLR p-value: | 0.003969 | ||||||

| coef | std err | z | P>|z| | [0.025 | 0.975] | ||||

| Abnormal | return | 60 day | 0.0078 | 0.006 | 1.292 | 0.196 | -0.004 | 0.02 | |

| Gross | Profit | Margin | 0.01 | 0.006 | 1.646 | 0.1 | -0.002 | 0.022 | |

| Profit | to | Capital | -1.3091 | 1.296 | -1.01 | 0.313 | -3.85 | 1.232 | |

| Return | on | Sales | -0.0185 | 0.009 | -2.015 | 0.044 | -0.036 | -0.001 | |

| EV | to | EBIDTA | -0.0004 | 0.005 | -0.075 | 0.94 | -0.01 | 0.009 | |

| Sales | growth, | 3y | 0.0055 | 0.005 | 1.17 | 0.242 | -0.004 | 0.015 | |

| Free | cash | Flow/Sales | 0.364 | 0.254 | 1.434 | 0.152 | -0.133 | 0.861 | |

| Current | Ratio | 0.2083 | 0.101 | 2.067 | 0.039 | 0.011 | 0.406 | ||

| Price | to | Sales | 0.0203 | 0.06 | 0.339 | 0.735 | -0.097 | 0.137 | |

| Market | to | Book | -0.0014 | 0.009 | -0.152 | 0.879 | -0.019 | 0.016 | |

| Debt | to | EV | 0.0046 | 0.005 | 0.892 | 0.372 | -0.006 | 0.015 | |

| Cash | to | Capital | -1.3762 | 1.377 | -0.999 | 0.318 | -4.076 | 1.323 | |

| Net | debt | per share | -0.0111 | 0.005 | -2.401 | 0.016 | -0.02 | -0.002 | |

| Growth-Resource | Mismatch | -0.3546 | 0.283 | -1.252 | 0.211 | -0.91 | 0.201 |

Furthermore, Model based on Cluster 1 data, which provides logistic regression outputs based on 442 low liquid and high-levered companies, suggests somewhat different results. Return on Sales proxying inefficient management is significant at 5% level and is in line with previous studies. The rest of the variables are insignificant except Net debt per share and Current ratios. It is worth mentioning that the coefficient for Net debt per share is negative, as was in Model based on Cluster 0 data. Moreover, the current ratio is significant at a 5% level, positively contributing to our earlier argument that observed target companies have higher liquidity.

print('\033[1m' + "Accuracy metrics for the model based on the entire dataset" + '\033[0m')

print('Classification accuracy: {:.3f}'.format(lr.score(X, y)))

print('ROC_AUC score: {:.3f}'.format(roc_auc_score(y, lr.predict_proba(X)[:, 1])))

print('\033[1m' + "\nAccuracy metrics for the model based on the Cluster 0 data" + '\033[0m')

print('Classification accuracy: {:.3f}'.format(lr_0.score(X.iloc[cl_0_idx], y.iloc[cl_0_idx])))

print('ROC_AUC score: {:.3f}'.format(roc_auc_score(y.iloc[cl_0_idx], lr_0.predict_proba(X.iloc[cl_0_idx])[:, 1])))

print('\033[1m' + "\nAccuracy metrics for the model based on the Cluster 1 data" + '\033[0m')

print('Classification accuracy on test set: {:.3f}'.format(lr_1.score(X.iloc[cl_1_idx], y.iloc[cl_1_idx])))

print('ROC_AUC score: {:.3f}'.format(roc_auc_score(y.iloc[cl_1_idx], lr_1.predict_proba(X.iloc[cl_1_idx])[:, 1])))

Accuracy metrics for the model based on the entire dataset

Classification accuracy: 0.575

ROC_AUC score: 0.602

Accuracy metrics for the model based on the Cluster 0 data

Classification accuracy: 0.595

ROC_AUC score: 0.618

Accuracy metrics for the model based on the Cluster 1 data

Classification accuracy on test set: 0.606

ROC_AUC score: 0.644

The comparison of the three models shows that Clustered models produce relatively better results according to the Accuracy, AUC measure, and Pseudo R squire. We believe that the AUC measure is a better estimate, considering that Clustered models are imbalanced, and equal to 0.6, 0.618, and 0.644 for Model 1, 2, and 3, respectively. Additionally, models on clustered data have better explanatory power as clustered models produced a more comprehensive view of significant variables. However, it is also worth noting that the difference in model accuracy is not radical and can be associated with the sample size, which is the smallest for Model 3. The difference becomes even smaller after the cross-validation. Results from stratified cross-validation with ten splits for accuracy and AUC scores are summarized in the table below.

cv = StratifiedKFold(n_splits=10)

# implement 10-k cross validation for each model

scores_acc = cross_val_score(lr, X, y, scoring = 'accuracy', cv = cv, n_jobs = -1)

scores_roc = cross_val_score(lr, X, y, scoring = 'roc_auc', cv = cv, n_jobs = -1)

print('\033[1m' + "Accuracy metrics for the model based on the entire dataset after 10-fold cross-validation" + '\033[0m')

print('Accuracy: %.3f (%.3f)' % (mean(scores_acc), std(scores_acc)))

print('ROC_AUC score: %.3f (%.3f)' % (mean(scores_roc), std(scores_roc)))

scores_cl_0_acc = cross_val_score(lr_0,X.iloc[cl_0_idx], y.iloc[cl_0_idx], scoring = 'accuracy', cv = cv, n_jobs = -1)

scores_cl_0_roc = cross_val_score(lr_0,X.iloc[cl_0_idx], y.iloc[cl_0_idx], scoring = 'roc_auc', cv = cv, n_jobs = -1)

print('\033[1m' + "\nAccuracy metrics for the model based on the Cluster 0 data after 10-fold cross-validation" + '\033[0m')

print('Accuracy: %.3f (%.3f)' % (mean(scores_cl_0_acc), std(scores_cl_0_acc)))

print('ROC_AUC score: %.3f (%.3f)' % (mean(scores_cl_0_roc), std(scores_cl_0_roc)))

scores_cl_1_acc = cross_val_score(lr_1,X.iloc[cl_1_idx], y.iloc[cl_1_idx], scoring = 'accuracy', cv = cv, n_jobs = -1)

scores_cl_1_roc = cross_val_score(lr_1,X.iloc[cl_1_idx], y.iloc[cl_1_idx], scoring = 'roc_auc', cv = cv, n_jobs = -1)

print('\033[1m' + "\nAccuracy metrics for the model based on the Cluster 1 data after 10-fold cross-validation" + '\033[0m')

print('Accuracy: %.3f (%.3f)' % (mean(scores_cl_1_acc), std(scores_cl_1_acc)))

print('ROC_AUC score: %.3f (%.3f)' % (mean(scores_cl_1_roc), std(scores_cl_1_roc)))

Accuracy metrics for the model based on the entire dataset after 10-fold cross-validation

Accuracy: 0.565 (0.033)

ROC_AUC score: 0.578 (0.040)

Accuracy metrics for the model based on the Cluster 0 data after 10-fold cross-validation

Accuracy: 0.570 (0.051)

ROC_AUC score: 0.572 (0.048)

Accuracy metrics for the model based on the Cluster 1 data after 10-fold cross-validation

Accuracy: 0.577 (0.070)

ROC_AUC score: 0.593 (0.073)

It should be noted that the current comparison is only preliminary, and actual accuracies will depend on how well the models will generalize on the hold-out sample, which is discussed later in this chapter. Nevertheless, higher accuracy and AUC measures of clustered models after cross-validation indicate that clustering will improve accuracy. To ensure the robustness of our claim, the hypothesis is also tested on a hold-out sample.

As mentioned earlier, the predictive power of the model is estimated on the hold-out sample consisting of target group observations after 2020-01-01 and all non-target peer companies. The hold sample includes 84 target and 1704 non-target companies The reason we test our model on highly unbalanced dataset is to to have a similar to natural world distribution of target and non-target companies.

To estimate the predictive power of the models, an optimal cut-off rather than an arbitrary one (0.5) needs to be identified. Considering that we aim to compare two models (general and clustered) a universal approach is suggested. Considering unbalanced datasets of clustered models and the one from the hold-out sample, the optimal cut-off for the models is derived G-measure approach which is the geometric mean of precision and recall. The formula is given as follows:

$$ \begin{array}{ll} {G}_{measure} = \sqrt{Recall * Specificity} = \sqrt{TPR * \frac {TN} {FP+TN}} \end{array}$$

where

$$ \begin{array}{ll} \sqrt{TPR * \frac {TN} {FP+TN}} = {(1 - \frac {FP} {FP + TN})} \end{array}$$

and finally: $$ \begin{array}{ll} {G}_{measure} = \sqrt{TPR * (1-FPR)} \end{array}$$

The cut-off is further used to classify companies and include in the portfolio. For the companies where target probability is bigger than the optimal cut-off model classifies as target and includes in the portfolio.

The following function allows to identify the optimal cut-off and highlights it in a plot.

def find_optimal_cutoff(model, X, y_true):

'''

Dependencies

------------

Python library 'Plotnine' version 0.8.0

Parameters

-----------

Identify optimal threshold for the model based on Youden’s J index and plot ROC curve

Input:

model: name of the model for which optimal threshold is being calculates

X (DataFrame): DataFrame of independent variables

y_true (Series): Series of True Labels

Output:

threshold_opt (Series): Series of True Labels

ROC curve

'''

# get target probabilities

lr_probs = model.predict_proba(X)

lr_probs = lr_probs[:, 1]

# create dataframe of TPR and FPR per threshold

fpr, tpr, thresholds = roc_curve(y_true, lr_probs)

df_fpr_tpr = pd.DataFrame({'FPR':fpr, 'TPR':tpr, 'Threshold':thresholds})

# calculate optimal threshold based on Gmean

gmean = np.sqrt(tpr * (1 - fpr))

index = np.argmax(gmean)

threshold_opt = round(thresholds[index], ndigits = 4)

gmean_opt = round(gmean[index], ndigits = 4)

fpr_opt = round(fpr[index], ndigits = 4)

tpr_opt = round(tpr[index], ndigits = 4)

print('Best Threshold: {} with G-Mean: {}'.format(threshold_opt, gmean_opt))

print('FPR: {}, TPR: {}'.format(fpr_opt, tpr_opt))

# plot the ROC curve and the optimal point:

# source of the visualization: https://towardsdatascience.com/optimal-threshold-for-imbalanced-classification-5884e870c293

pn.options.figure_size = (6,4)

return threshold_opt, (

ggplot(data = df_fpr_tpr)+

geom_point(aes(x = 'FPR',

y = 'TPR'),

size = 0.4)+

geom_point(aes(x = fpr_opt,

y = tpr_opt),

color = '#981220',

size = 4)+

geom_line(aes(x = 'FPR',

y = 'TPR'))+

geom_text(aes(x = fpr_opt,

y = tpr_opt),

label = 'Optimal threshold: {}'.format(threshold_opt),

nudge_x = 0.14,

nudge_y = -0.10,

size = 10,

fontstyle = 'italic')+

labs(title = 'ROC Curve')+

xlab('False Positive Rate (FPR)')+

ylab('True Positive Rate (TPR)')+

theme_minimal()

)

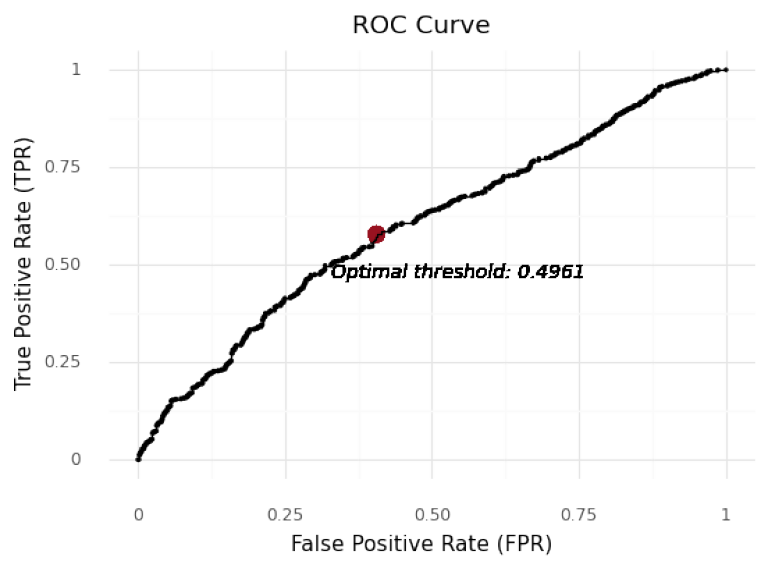

First we identify the optimal cut-off for the model based on the entire dataset using the function above.

# get threshold for Model 1 and plot the ROC curve

threshold_opt, plot = find_optimal_cutoff(lr, X, y)

plot

Best Threshold: 0.4961 with G-Mean: 0.5865

FPR: 0.4056, TPR: 0.5787

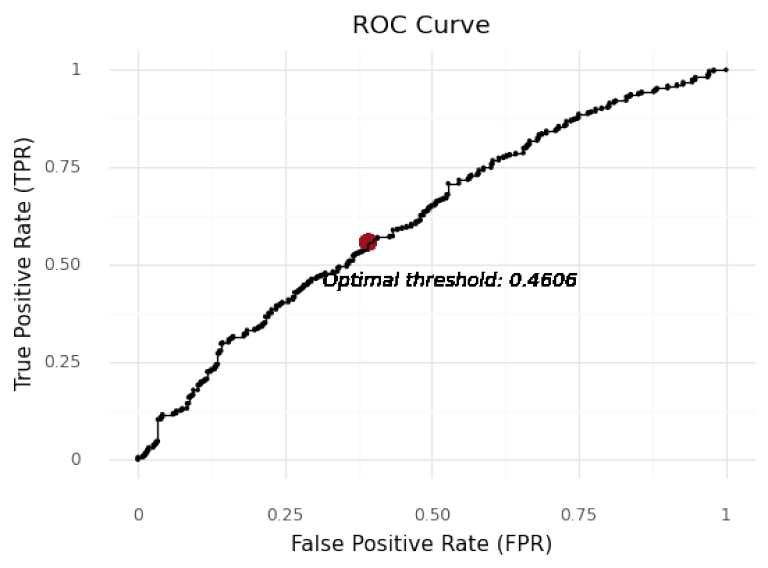

Then we identify the optimal cut-off for the model based on the cluster 0 data.

threshold_opt_cl_0, plot_cl_0 = find_optimal_cutoff(lr_0, X.iloc[cl_0_idx], y.iloc[cl_0_idx])

plot_cl_0

Best Threshold: 0.4606 with G-Mean: 0.5826

FPR: 0.3916, TPR: 0.558

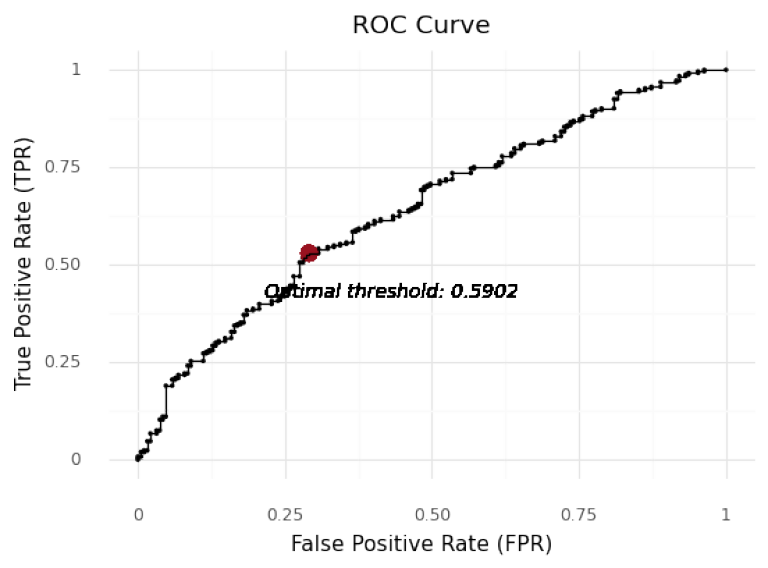

threshold_opt_cl_1, plot_cl_1 = find_optimal_cutoff(lr_1, X.iloc[cl_1_idx], y.iloc[cl_1_idx])

plot_cl_1

Best Threshold: 0.5902 with G-Mean: 0.6128

FPR: 0.291, TPR: 0.5296

By employing this methodology, cut-off points of 0.4961, 0.460 and 0.5901 are determined for unclustered and cluster 0 and cluster 1 models respectively. The cut-offs mentioned above are employed to evaluate the predictive ability of the models, including Accuracy to determine how well the models identify actual targets and non-targets, Precision, Recall (TPR), and FPR to get further deeper insight on each aspect of the prediction as well as F1 score to evaluate the overall quality of different models.

First we divide the holdout sample into dependent and independent variables

# drop to be removeded variables from hold-out sample

data_hold.drop(columns = drop, inplace = True)

# Separate independent and dependent variables

X_test = data_hold.drop(['AD-30', 'Announcement Date', 'Label',"Company RIC",'Market Cap','Total debt to Equity'], axis = 1)

y_test = data_hold['Label']

X_test.head()

| Abnormal return 60 day | Gross Profit Margin | Profit to Capital | Return on Sales | EV to EBIDTA | Sales growth, 3y | Free cash Flow/Sales | Current Ratio | Price to Sales | Market to Book | Debt to EV | Cash to Capital | Net debt per share | Growth-Resource Mismatch | |

| 0 | -9.775437 | 59.18308 | 0.077847 | 4.544522 | 65.10298 | 0.521386 | 0.096377 | 1.38192 | 4.807378 | 11.428748 | 0.996802 | 1.002554 | -6.270184 | 1 |

| 1 | -7.701835 | 33.81626 | 0.0565 | 7.288653 | 40.759031 | -2.363193 | 0.112886 | 2.69199 | 4.424246 | 4.644855 | 0.180739 | 0.098591 | -0.842171 | 1 |

| 2 | -11.843083 | 18.96168 | -0.139595 | 2.823379 | 11.659163 | 3.438428 | 0.053293 | 1.86214 | 0.813417 | 2.430913 | 32.008828 | 0.193466 | 9.432784 | 1 |

| 3 | -11.146474 | 32.09241 | 0.058989 | 7.49143 | 7.752199 | 2.581302 | 0.071953 | 1.89468 | 0.931876 | 1.780169 | 3.052414 | 0.107747 | -1.440183 | 0 |

| 4 | -9.647523 | 8.89214 | -5.337401 | -20.078817 | 113.200436 | 14.994174 | -0.007138 | 0.52276 | 7.253047 | 45.870267 | 1.849967 | 0.044645 | 0.080742 | 0 |

# get target probabilities

prob = lr.predict_proba(X_test)

# create dataframe and store model results

pred_res_lr = data_hold[['Announcement Date','Company RIC','Label']]

pred_res_lr.insert(loc = len(pred_res_lr.columns), column = "Probability_target", value = prob[:,1])

pred_res_lr.insert(loc = len(pred_res_lr.columns), column = "Class", value = np.where(pred_res_lr['Probability_target'] > threshold_opt, 1, 0))

# assign TP/FP/TN/FN labels based on the specified cut-off probability

pred_res_lr.insert(loc = len(pred_res_lr.columns), column = "Outcome", value =

np.where((pred_res_lr['Class'] == 1) & (pred_res_lr['Label'] == 1), "TP",

np.where((pred_res_lr['Class'] == 1) & (pred_res_lr['Label'] == 0),"FP",

np.where((pred_res_lr['Class'] == 0) & (pred_res_lr['Label'] == 1),"FN", "TN"))))

pred_res_lr.head()

| Announcement Date | Company RIC | Label | Probability_target | Class | Outcome | |

| 0 | 28/06/2021 | QADA.O | 1 | 0.403778 | 0 | FN |

| 1 | 21/06/2021 | RAVN.O | 1 | 0.367537 | 0 | FN |

| 2 | 21/06/2021 | LDL | 1 | 0.487374 | 0 | FN |

| 3 | 18/06/2021 | SYKE.OQ^H21 | 1 | 0.416753 | 0 | FN |

| 4 | 08/06/2021 | MCF | 1 | 0.971662 | 1 | TP |

print('\033[1m' + "Observations" + '\033[0m')

print(f'Total Number of companies: {pred_res_lr.shape[0]}')

print('Number of target companies: ' + str(pred_res_lr.loc[pred_res_lr['Label'] == 1].shape[0]))

print('Number of non-companies: ' + str(pred_res_lr.loc[pred_res_lr['Label'] == 0].shape[0]))

# calculate confusion matrix data based on specified cut-off probability

TP_lr = pred_res_lr.loc[pred_res_lr['Outcome'] == "TP"].shape[0]