Article

Debt Structure Analysis on an Organizational Level

Many times when one is looking to analyze the Debt Structure of an issuer within the desktop using Refinitiv Workspace / Eikon, the first thought is to look at the Debt Structure page. This is an excellent resource to analyze all bonds that meet specific requirements be it Maturity, Capital Tier, Coupon Class amongst many other categories. Not only does this information give us insight into the debt obligations of said organization, but it also sheds light on the burdens of future coupon payments, the distribution of risk, and the implications in new areas such as Green Bonds.

With this article, we would like to bring this kind of analysis to life through the use of the Refinitiv Data Platform Library and the Eikon Data API. We will go through some simple steps to search for all the bonds for a given issuer, look at some of the most relevant fields for the active bonds, and we will standardize the currency so we can look at the total value of the obligations in a single currency. This is done with the intent of explaining how to use the Search API functionality, how we can organize the properties/fields we're interested in, how to implement FX conversion from the currency of issue to a chosen FX snapshot, and then ultimately look at the overall obligations by subsidiary but also as a whole

Getting Started

To get started we will need to import the Refinitiv Data Platform API as well as the Eikon Data API. We are also importing pandas for data frame management.

import refinitiv.dataplatform as rdp

import refinitiv.dataplatform.eikon as ek

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

# Open a session into the desktop.

rdp.open_desktop_session('DEFAULT_CODE_BOOK_APP_KEY')

Company Selection

The following procedures can be used to determine the company of interest based on its Organization ID, or Company Perm ID. Within the desktop, there are a few ways to acquire the ID. In each case, you can search for the name of the company and look for the ID as follows:

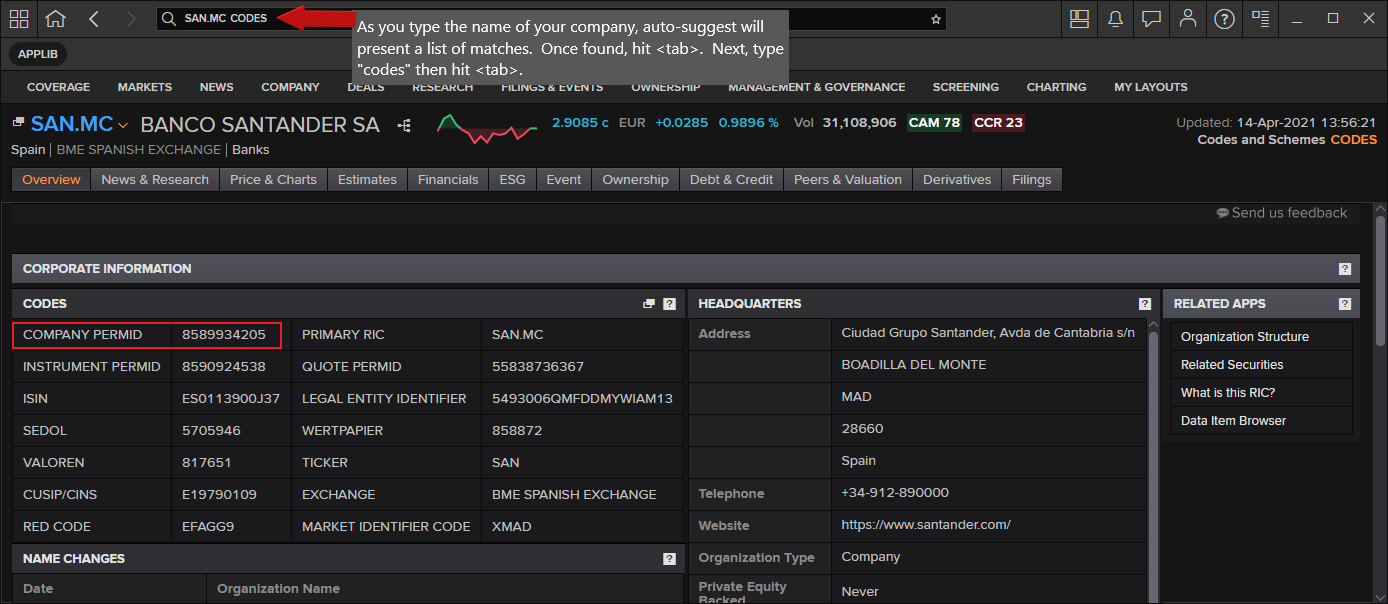

- From the search window in the Desktop Taskbar, start typing the name of the company. For example, using Refinitiv Workspace, start typing and auto-suggest will present matches. When found, hit the "tab" key. Then, type codes and hit tab again and the following screen should appear:

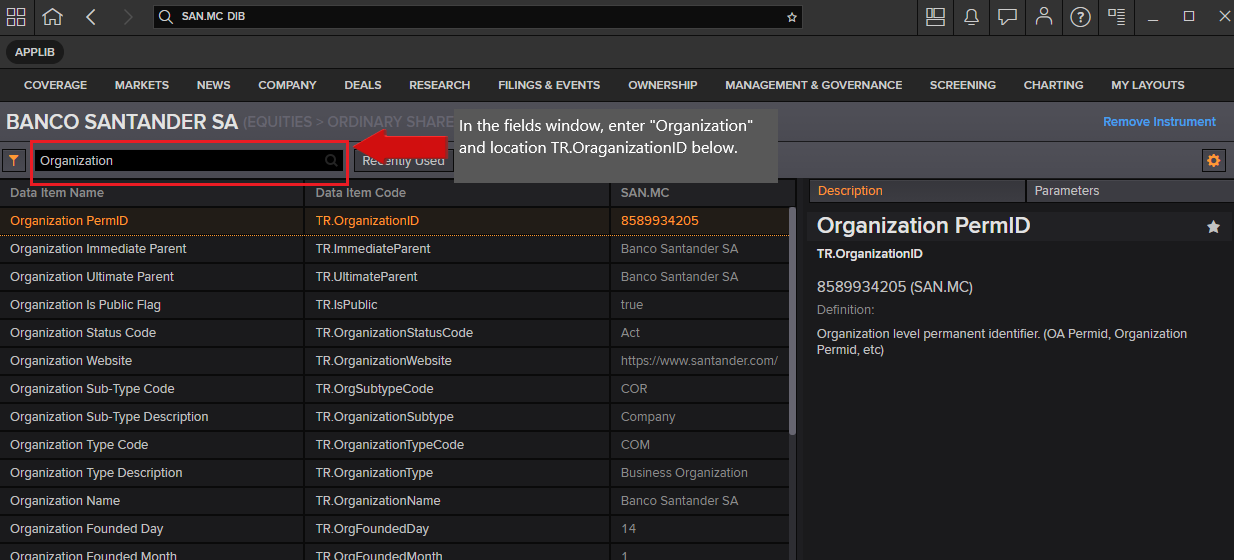

- Within the desktop, pull up the DIB (Data Item Browser) and locate the field [TR.OrganizationID]. For example, as above, select the company. In the field input window, type "Organization" and look for TR.OrganizationID.

- Programmatically, you can determine the ID when providing the company Name.

# Determine the organization ID using Search.

rdp.search(

view = rdp.SearchViews.GovCorpInstruments,

top = 5,

query="Santander",

select = "ParentOAPermID"

)

Once determined, assign the value below that will be named 'org_id' in our code going forward.

Note: We could possibly use the company name as the search criteria in our main searching of bonds, as opposed to finding the organization id, but we want to ensure we're referring to the actual company as opposed to the possibility of returning results that closely match based on the company expression provided.

# Define the Organisation ID / Perm ID as the basis of our search to pull out the collection of bonds

org_id = "8589934205" # Banco Santander

Present the company name.

Using the RDP Search service, query for the specified organization to retrieve the full parent name. We'll use this as a simple title for our presentation chart.

company = rdp.search(query=org_id, select="DTSubjectName")

company

Debt Structure

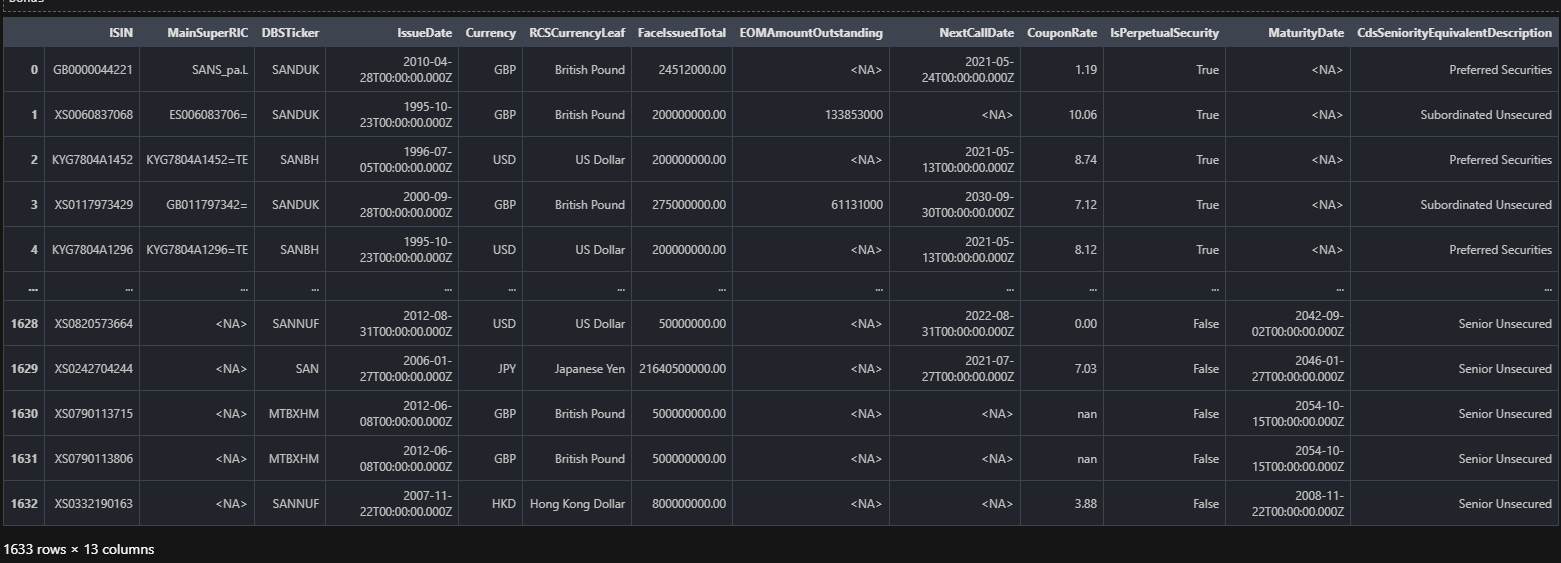

The following request utilizes the RDP Search call to select the list of bonds associated with the defined company. When searching for bonds, we must define criteria where the state of the bond is active. For each bond, we pull out a set of properties, or fields, that are relevant for our collection. Most notably, we choose some critical values such as the Amount Oustanding, Coupon Rate, and Total Face Value Issued for the bond. In addition, we must add the currency of each bond, as this is ultimately the determining factor when we standardize a specified currency for the values selected.

The rdp.search() API call is a powerful utility offering detailed search analysis that developers can customize for their requirements. The output, i.e. columns or fields returned, is based on the select parameter - see below. The specific selection of these properties has been determined by utilizing Search metadata analysis and debugging features. These features provide the ability to interrogate the values returned, allowing the user to determine the desired properties. For additional details around Search and how to get the most out of this service, refer to the Building Search into your Application Workflow article.

First, define the output fields/properties of interest. In the article mentioned above, you will find the steps to finding the entire universe of properties/fields (what we know as Data Items in Eikon) for the universe you're looking at. In this case, we are looking at GovCorpInstruments and have chosen a handful of properties to include.

# Define the collection of properties/fields within our result set

properties = ['ISIN', 'MainSuperRIC', 'DBSTicker', 'IssueDate', 'Currency', 'RCSCurrencyLeaf',

'FaceIssuedTotal', 'EOMAmountOutstanding', 'NextCallDate', 'CouponRate',

'IsPerpetualSecurity', 'MaturityDate', 'CdsSeniorityEquivalentDescription']

# Populate empty columns

# In some cases, depending on the specified company, the result set may contain unavailable columns

# of data within the result set. The following logic will ensure our results will contain the necessary

# columns of data.

def populate_empty_columns(df):

for prop in properties:

if (prop not in df):

df[prop] = pd.NA

df = rdp.Search.search(

# The 'view' represents a specific domain of content we wish to search across.

view = rdp.SearchViews.GovCorpInstruments,

# The 'filter' parameter is a powerful, criteria-based, syntax that allows us to filter for specific

# results.

#

# Note: The expression below utilizes a convenient, modern Python syntax called

# 'String interpolation'.

#

# This feature utilizes f-strings to embed arguments within the string result.

# Refer to the site: https://www.programiz.com/python-programming/string-interpolation for more

# details.

#

# Disclaimer: The following expression includes bonds that are in 'default'. If you choose to ignore

# these from your result set, simply modify the expression below as follows:

#

# "..not(AssetStatus in ('MAT' 'DEF'))"

#

filter = f"ParentOAPermID eq '{org_id}' and IsActive eq true and not(AssetStatus in ('MAT'))",

# Define the upper limit of rows within our result set. This is a system imposed maximum value.

top = 10000,

# The 'select' parameter determines the fields of interest in our output. The logic below takes our

# list of properties defined and creates the appropriate comma-separated list of properties required

# by the service.

select = ','.join(properties),

# The navigator will list all the unique currencies associated with the result set. Used below for

# conversion.

navigators = "Currency"

)

# Bonds represents a simple reference to our data

bonds = df.data.df

# When using search, the order of the columns in our result set are not ordered based on the properties

# defined within the above 'select' statement. As a result, I will re-order them for a more intuitive

# display.

#

# Before I reorder them, I will need to ensure our columns exist.

populate_empty_columns(bonds)

# Now we can re-order the columns

bonds = bonds[properties]

bonds

Currency Conversion

Looking at the above display, the set of bonds returned may be represented in multiple currencies. The goal of our exercise is to standardize our numeric values based on a selected, base Currency. For example, we may choose to have all values within the result set to be represented in the Euro (EUR).

In the above request, we have utilized the navigators parameter when performing our search. This parameter provides a convenient way to collect and bucket all currencies within our search output. By doing this, I can walk through this collection and perform a conversion to a selected base currency and capture the conversion factors within a conversion table. In a later step, the table can then be used to convert the numeric values for each bond we selected.

The code below performs the conversion in a 2-step process.

Retrieve the Currency Conversion factor

Refinitiv has created a number of convenient Cross Rate instrument codes exclusively designed to retrieve a conversion value that can be used as the basis for conversion. For example, the following Cross Rate code converts from the British Pound to Euro:

GBPEUR=R

The algorithm below derives the code from the source currency, eg: 'GBP', and the base currency (what we want to convert to), eg: 'EUR'. The conversion value returned may require additional factoring based on a Scaling factor. When retrieving the conversion value, we also retrieve a scaling factor that we must apply an additional calculation. For example, a cross rate code may return a scaling factor of 1, where another may return a scaling factor of 100. In either case, I must apply a final calculation as:

Conversion Factor = Conversion value / Scaling factor

Optionally, derive Currency Conversion factor

In some cases, there may be no Cross Rate instrument code defined, depending on the source currency and/or the base currency. As such, the algorithm will manually create the conversion factor by deducing both the source currency rate, eg: 'GBP=', and the base currency rate: 'EUR=' and perform a simple calculation to derive the Cross Rate factor.

The result of the following functionality is to produce a conversion table, keyed on the source currency code, that allows simple access to the conversion factor for a selected base currency.

# assign_rates

# During step 1 of the conversion process, I walk through the results of attempting to retrieve a

# conversion factor for the constructed Cross Rate codes. The algorithm will map out those factors

# we found and those factors which are not available/missing. If we have found any missing entries,

# I use them in step 2 (assign_missing).

def assign_rates(row, table, missing):

currency = row['Currency']

if row.isna()['PRIMACT_1']:

missing.add(f'{currency}=')

else:

table[currency]['rate'] = row['PRIMACT_1'] / row['SCALING']

# assign_missing

# If we discovered any missing conversion rates, based on our constructed Cross Rate instrument codes,

# we now have the opportunity to manually derive the conversion factor based on a 'base' conversion

# factor and the currency rate for each missing entry.

def assign_missing(row, table, base):

instrument = row['Instrument']

currency = instrument[:-1]

if not row.isna()['PRIMACT_1'] and currency in table:

if table[currency]['rate'] == 0:

table[currency]['rate'] = base / row['PRIMACT_1']

# build_cross_rate_table

# In this function, I perform the following logic:

#

# 1. Construct the Cross Rate instrument codes

# 2. Based on the list of codes, utilize the Eikon Data API to retrieve the conversion factor

# (assign_rates)

# 3. If I discovered we are missing some conversion factors, construct the list of missing currencies

# 4. For each missing currency, utilize the Eikon Data API to retrieve the currency rates

# 5. Based on the results, and the result of the base currency rate, assign the missing conversion

# rates (assign_missing)

def build_cross_rate_table(data, to_currency):

table = {}

spots = []

currencies = []

# Iterate through the array of currency codes, defining the cross rates...

for node in data:

table_node = {}

currency = node['Label']

if currency != to_currency:

table_node = {'rate': 0, 'base': to_currency}

table[currency] = table_node

spots.append(f'{currency}{to_currency}=R')

currencies.append(currency)

# The currencies table represents the list of items we intend on retrieving the spot rates

rates,err = ek.get_data(spots, ['PRIMACT_1', 'SCALING'])

tmp = pd.DataFrame({'Instrument': spots, 'Currency': currencies})

rates = rates.set_index("Instrument").join(tmp.set_index("Instrument"))

# Assign the results to our conversion table

missing_values = set()

rates.apply(assign_rates, args=[table, missing_values], axis=1)

# For those spot rate requests that did not return a value, this was likely due to the fact that

# the derived item was not defined in the backend. As a result, I will need to derive the

# value based on a manual cross rate conversion.

if len(missing_values) > 0:

base = f'{to_currency}='

missing_values.add(base)

rates,err = ek.get_data(list(missing_values), ['PRIMACT_1', 'SCALING'])

# For the missing values, apply a manual conversion based on the computed value for the base

# currency

rates.apply(assign_missing, args=[table, rates.loc[rates['Instrument'] == base]

['PRIMACT_1'].values[0]], axis=1)

# The resulting table represents our conversion factors for each currency within the result set

return table

to_currency ='EUR'

conversion_table = build_cross_rate_table(df.data.raw['Navigators']['Currency'] ['Buckets'], to_currency)

conversion_table

{'USD': {'rate': 0.8345, 'base': 'EUR'},

'CLF': {'rate': 34.749, 'base': 'EUR'},

'CLP': {'rate': 0.001176, 'base': 'EUR'},

'GBP': {'rate': 1.15, 'base': 'EUR'},

'COP': {'rate': 0.00022810000000000001, 'base': 'EUR'},

'JPY': {'rate': 0.007659999999999999, 'base': 'EUR'},

'MXN': {'rate': 0.04155, 'base': 'EUR'},

'NOK': {'rate': 0.0995, 'base': 'EUR'},

'AUD': {'rate': 0.6447, 'base': 'EUR'},

'CHF': {'rate': 0.9041, 'base': 'EUR'},

'SEK': {'rate': 0.0986, 'base': 'EUR'},

'PEN': {'rate': 0.2296, 'base': 'EUR'},

'PLN': {'rate': 0.2193, 'base': 'EUR'},

'RON': {'rate': 0.2029, 'base': 'EUR'},

'ARS': {'rate': 0.009000000000000001, 'base': 'EUR'},

'CZK': {'rate': 0.03852, 'base': 'EUR'},

'DKK': {'rate': 0.134441, 'base': 'EUR'},

'HKD': {'rate': 0.107449, 'base': 'EUR'},

'BRL': {'rate': 0.1475, 'base': 'EUR'}}

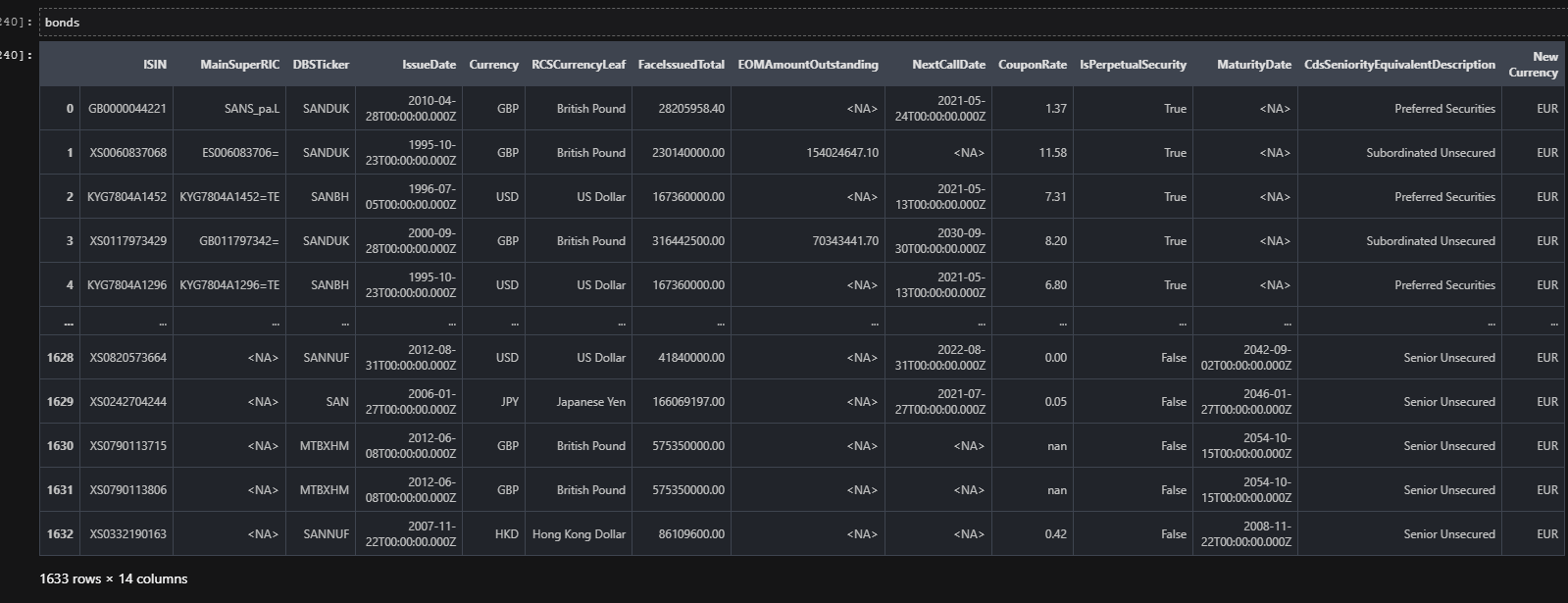

def convert_currency(cell, node):

if (isinstance(cell, (int, float)) and not isinstance(cell, bool)):

cell = cell * node['rate']

return cell

def process_row(row, table):

# Retrieve the currency code for this row

currency = row['Currency']

# Create a new column showing the new currency

base = ""

# Find this currency within the currency table

if (currency in table):

# Retrieve the currencies details from our conversion table

node = table[currency]

row['New Currency'] = node['base']

return row.apply(convert_currency, args=[node])

else:

row['New Currency'] = currency

return row

# The following call walks through the entire bond dataframe, and applies a conversion factor

# (convert_currency) to the relevant values for each row (process_row).

# The 'conversion_table' contains the conversion factors for each currency.

bonds = bonds.apply(process_row, args=[conversion_table], axis=1)

# Define our dataframe options with use of pandas formatting to give us 2 decimal places for our

# floating data

pd.options.display.float_format = '{:.2f}'.format

Visualization and analysis of results

It's great to see how straightforward it has been to pull up the bonds that met the requirements, make sure the data is properly populated, format the floating results to a standard 2 decimals, and display them in their newly standardized currency.

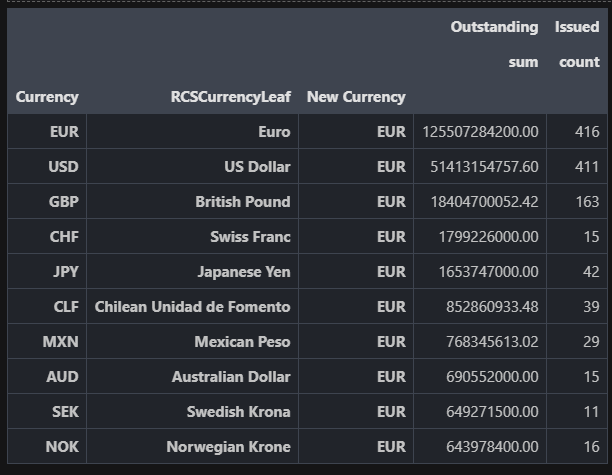

With this done, let's look at totals, and a simple chart to get a broad idea of which subsidiary owes what, what the Rank is of each of the bonds, and how they contribute to the big picture of the organizations' debt structure.

# Present a table, ranked by the amount outstanding. Include the # issued for each currency.

table = (bonds.groupby(['Currency', 'RCSCurrencyLeaf', 'New Currency'])

.agg({

'EOMAmountOutstanding': ['sum'],

'ISIN': ['count']

})

).sort_values([('EOMAmountOutstanding', 'sum')], ascending=False)

# For display purposes, grab the top 10 and rename the column labels

plt_table = table.head(10).rename(columns={'EOMAmountOutstanding': 'Outstanding', 'ISIN': 'Issued'})

plt_table

# Plot the data

plt.rcParams['figure.figsize'] = (13,7)

fig, ax = plt.subplots()

ax.tick_params(labelrotation=90)

ax.bar(

x=np.arange(plt_table.shape[0]),

height=plt_table['Outstanding', 'sum'],

tick_label=plt_table.index.get_level_values(1),

alpha=0.5

)

# Remove the spines from the graph - leave the bottom

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

ax.spines['left'].set_visible(False)

ax.tick_params(bottom=False, left=False)

# Add a faint grid

ax.yaxis.grid(True, alpha=0.1)

ax.xaxis.grid(True, alpha=0.1)

# Add labels and a title. Note the use of `labelpad` and `pad` to add some

# extra space between the text and the tick labels.

ax.set_ylabel('Outstanding', labelpad=15, fontsize=16, color='cyan')

ax.set_title(f"Currency [{to_currency}] -- ({company['DTSubjectName'][0]})", pad=15, fontsize=16,

color='cyan')

fig.tight_layout()

Conclusions

In this simple yet constructive article, we have looked at how to use the APIs to search for active bonds for a company, bring back specific properties for the same, and then convert them all into a single currency so we are able to look at the whole picture. The currency conversion done in this article is transferrable to any asset class and any data set. Furthermore, the visualization in a table and chart is useful to get the 'quick big picture' in a large range of use cases. Look out for an article from the same authors on cash flow analysis for a portfolio of bonds where we'll be looking at expected cash flows, pay dates, and much more - all with the use of the basic tips you've learned here.

Source Code

Documentation